US consumers now carry fewer than 4 credit cards on average

Canva

US consumers now carry fewer than 4 credit cards on average

A close-up photograph of credit cards inside a wallet.

Many consumers may remember receiving their first credit card, either years ago in a plain envelope, or months ago from a smartphone app. Still other consumers may remember their newest card, maybe because it’s the credit card they’re now using exclusively to maximize cash back rewards or airline miles.

But for most consumers, there’s also a murky in-between where they add, drop and generally accumulate credit cards over time. Over the years, consumers may close some credit card accounts or leave some of their credit cards dormant as a backup form of payment, or perhaps left forgotten in a desk drawer.

In the data below, Experian reveals the changes in consumers wallets in recent years.

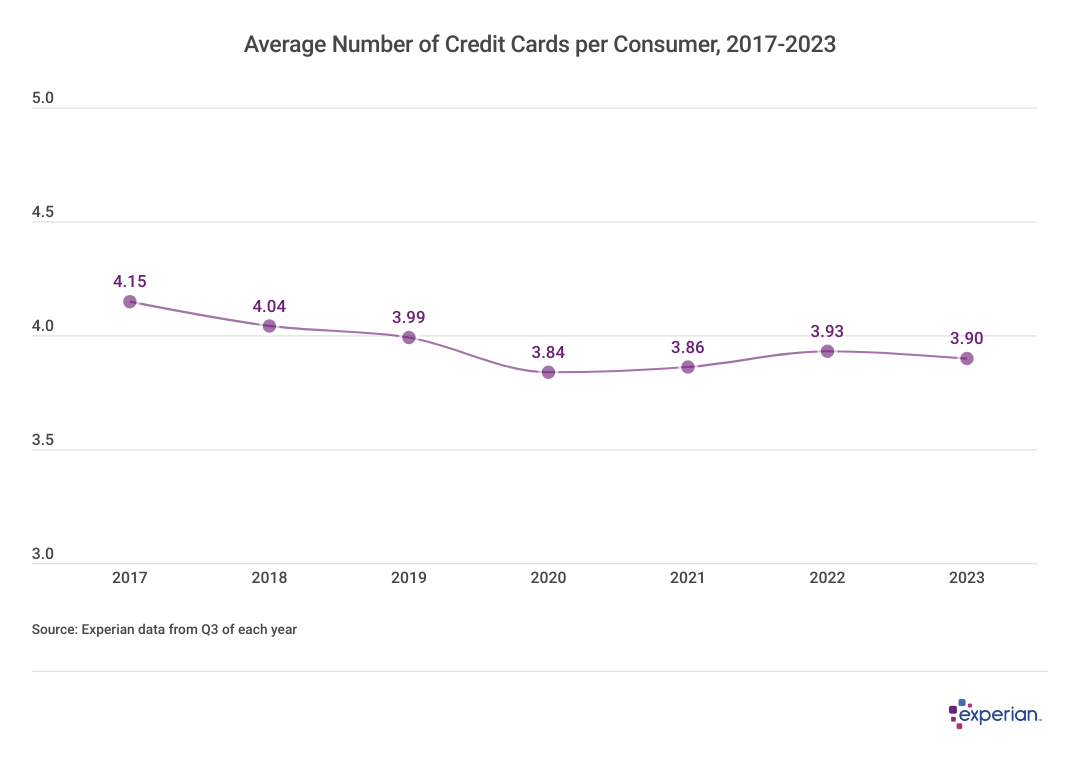

Average Number of Cards Has Declined Since 2017

U.S. consumers, on average, carry fewer cards today than they did in 2017, when the typical wallet held 4.2 active credit cards. As of the third quarter (Q3) of 2023, consumers carried 3.9 cards on average. This average is up slightly since the early days of the pandemic, when consumers reduced their average credit card debt and number of accounts as the economy slowed.

![]()

Experian

Number of Credit Cards Carried Drops Throughout the Years

Graph showing “Average Number of Credit Cards per Consumer, 2017-2023”.

As Experian revealed earlier this year, credit card balances are still climbing, despite (and partially because of) higher interest rates. And while average balances are increasing, they are spread across fewer accounts than in recent years. Alternative financing—including buy now, pay later plans for purchases—may account for at least some of this discrepancy, as consumers gravitate toward these newer financing methods.

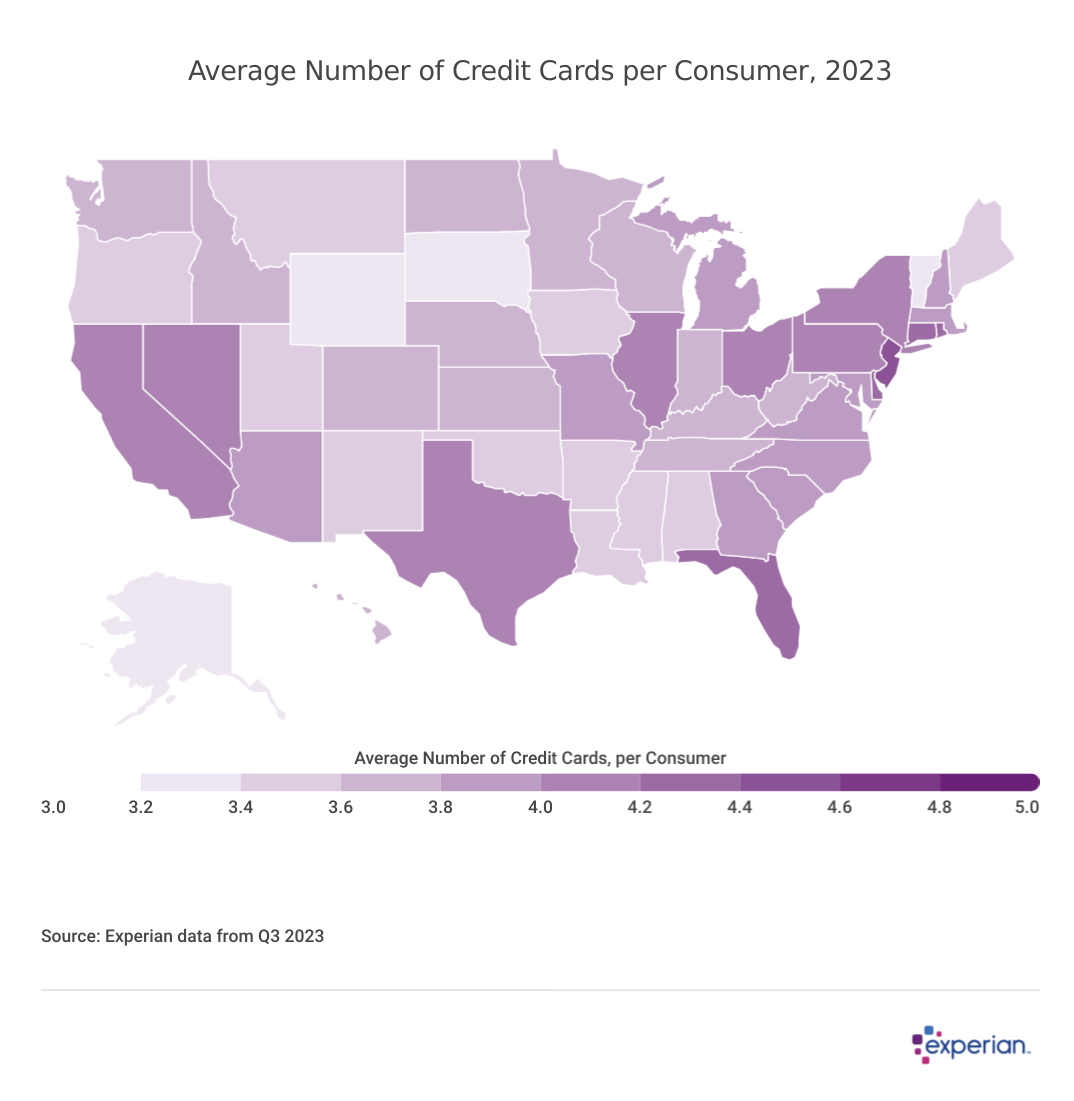

Residents of More Populous States Have More Credit Cards on Average

In general, residents of higher-population states tend to carry more credit cards than those who live in states with fewer and smaller population centers. Nonetheless, the difference between the states is relatively small. Considering that the national average is around four credit cards per consumer, the four states with the fewest cards per consumer (Alaska, South Dakota, Vermont and Wyoming) aren’t appreciably different, with “only” about 3.3 credit cards per consumer.

Experian

Average Number of Credit Cards Per Consumer is Similar Across the U.S.

Map showing results for “Average Number of Credit Cards per Consumer, 2023”.

Similarly, the four states on the higher end of the scale where consumers have 4.2 or more credit cards are Connecticut, Delaware, Florida, New Jersey and Rhode Island.

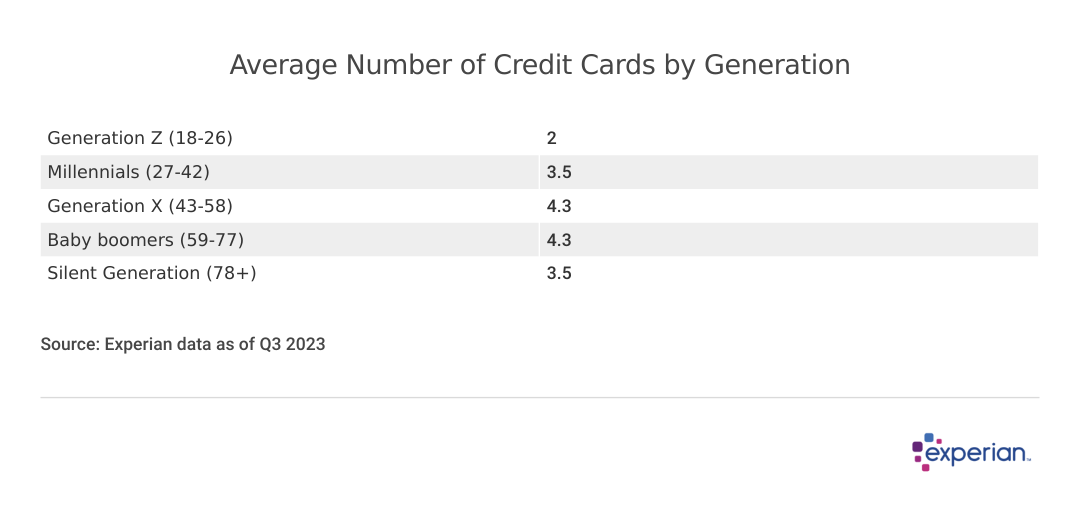

Older Consumers Have More Active Credit Cards on Average

The disparity in average credit card counts is more apparent when the population is segmented by age, thanks in part to Generation Z, many of whom have yet to receive their first credit card. The average number of credit cards for these consumers was two, less than half of what older generations keep on hand.

Experian

Number of Cards Carried Increases Into Middle Age

Table showing results of “Average Number of Credit Cards by Generation”.

The average number of credit cards held by each generation follows the familiar pattern seen in credit card balances, which tend to increase in a consumer’s middle age. It’s not surprising that the number of credit card accounts follows a similar climb throughout young adulthood and middle age, then drops off in the retirement years.

How Many Credit Cards Is Too Many?

No matter how many credit cards you may have at the moment, keep in mind that the number of accounts has little if any bearing on one’s FICO Score. Far more important is how consumers manage those accounts.

This is easily demonstrable by quickly stepping through some of the factors that affect your credit scores.

- Utilization and amounts owed: Credit card issuers extend credit to consumers in the form of a credit limit. Generally, the lower a consumer’s credit utilization, or balance compared with credit limit, the better. Keeping credit utilization ratios under 30% can lessen the negative impact credit card balances have on scores, and those with the highest credit scores tend to have credit utilization ratios in the low single digits. Conversely, carrying balances that begin to approach one’s credit limits may have adverse effects on credit scores.

- Delinquencies and payment history: As important as managing balances is, making payments on existing accounts has an even greater impact on scores. Even a single delinquency (late payment) may have an adverse effect on your credit score, no matter how few or many credit card accounts you have.

- Average age of accounts: This is the only credit score factor where the number of cards one carries may influence their credit score. However, even here, keeping older credit cards open is far from a clear-cut decision.

Longer credit histories do tend to have a positive effect on a consumer’s credit score, but it’s not something you can rush. Adhering to on-time payments and managing amounts owed will go far in improving credit scores, even absent a lengthy credit history. While accounts closed in good standing remain on your credit report for 10 years, canceling your oldest credit card account still has the potential to shorten your credit history when it is eventually removed. The impact of its removal depends on any other active credit cards in your credit file.

The Bottom Line

Ultimately, the number of cards a particular individual carries is a personal decision. Justifications can be found for carrying a travel rewards card, a cash back card, a balance transfer card, a card for business transactions and other types of credit cards that other consumers may not have either the need or qualifications for.

However, keeping track of numerous credit cards, whether or not a consumer is actively using all of them, can be a mentally taxing exercise. Not only that, credit card fees can add up and dull the benefit of carrying several credit cards. Organized consumers can benefit greatly from a wallet full of specialized cards, but for those seeking a more zen-like financial future, some judicial pruning may be in order.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.