Gen Z credit scores on the rise along with debt balances

Milan Ilic Photographer // Shutterstock

Gen Z credit scores on the rise along with debt balances

Two Gen Z women are engaged in a discussion while using a laptop.

The media is having a hard time nailing down the financial vibes of the youngest generation of consumers—Gen Z. You might see Gen Z described as financially unsure and insecure, knee deep in debt or even more spendy and carefree than the avocado toast generation that preceded them.

Despite the commentary, however, Experian data shows that by and large, Generation Z’s debt is increasing at the same rate as other generations’. As part of our ongoing review of consumer debt and credit in the United States, Experian took a look at the leading edge of Generation Z, who were between 18 and 26 years old in the third quarter (Q3) 2023. This analysis lays out some of the facts from aggregated Experian data, along with some context, to explain what’s happening in the wallets of younger consumers.

![]()

Experian

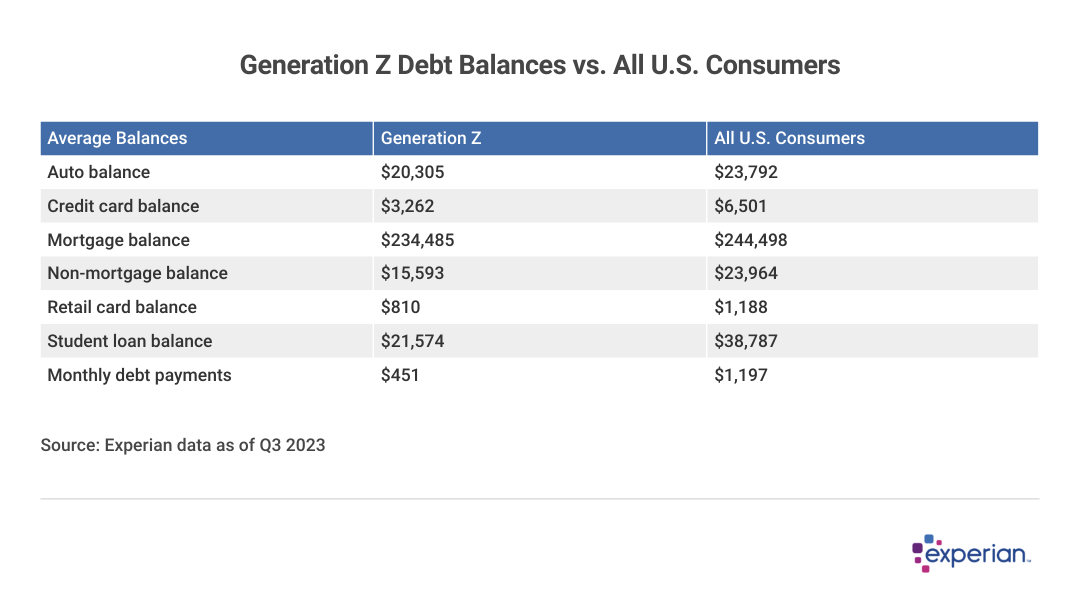

How Much Debt Does Gen Z Have?

Table showing “Generation Z Debt Balances vs. All U.S. Consumers”.

Gen Z isn’t falling into more debt than others, according to Experian data. Nor are comparisons to millennials at their age particularly apt, as 15 years ago the economic and credit landscape (both still reeling from the Great Recession) meant a different experience for both borrowers and lenders than what consumers face in the 2020s. Now, inflation and cost of living are contributing to increased debt balances—for Gen Z as well as for all consumers.

For some types of consumer debt, Gen Z balances are about half that of the overall consumer population. Even average student loan balances, a category you might think the youngest generation must have more of than other cohorts, is only half the U.S. average. (Think about how long and expensive grad school can be to explain the difference.)

It’s the big-ticket items, including a car and a house, that Gen Z can’t dodge. Among young consumers with an auto loan, the average balance of $20,305 is similar to the $23,792 national average. And among the few members of Generation Z who’ve recently bought their (presumably) first home, they’re carrying nearly as much mortgage debt as other homeowners.

Experian

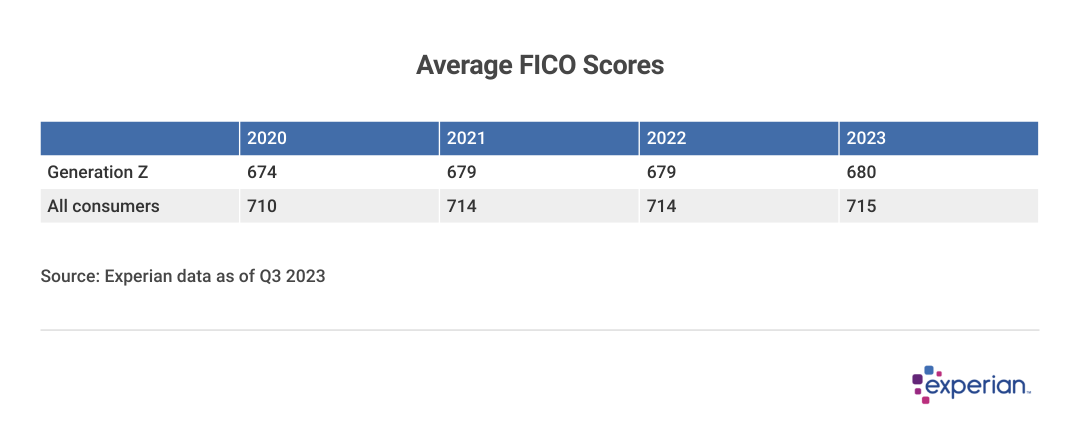

Average Gen Z Credit Scores Continue to Rise

Table showing “Average FICO Scores”.

The average FICO Score among Generation Z was 680 in Q3 2023. While this score puts them 35 points short of the national average credit score of 715, it lands them in the “good” FICO Score range, which starts at 670.

There’s no evidence, and little reason, to expect that one generation is more or less responsible with their credit than others, and that includes Generation Z. Factors that could cause average credit scores to drop are largely economically driven, and right now unemployment rates have been at or near the record low rates: less than 5% in nearly every state, and 3.9% nationwide. Unless unemployment rates somehow impact one generation more than another—extremely unlikely—there’s no reason to expect that one generation will zig while all the other zag.

However, that’s not to say the economic challenges each generation faces are the same—far from it. FICO Scores are a measure to assess risk, but not wealth.

Experian

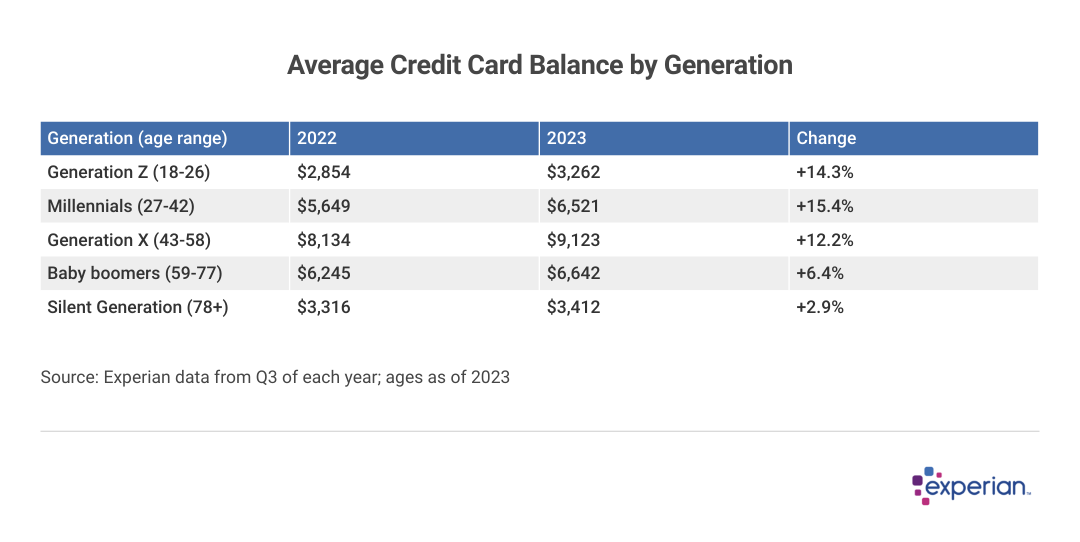

Most Gen Z Consumers Have a Credit Card, Lower Balances

Table showing “Average Credit Card Balance by Generation”.

As of Q3 2023, 86% of Gen Z consumers who have a credit score have at least one credit card, according to Experian data. And they’re beginning to use some of the credit extended to them.

Although inflation contributed to higher balances for U.S. consumers of all ages, the year-over-year increase is typically going to be greater for those starting from zero, as many Gen Zers obtaining their first credit card are doing. Even so, Generation Z’s balances grew just as much as other working-age consumers—millennials and Generation X. Consumers of any age who manage their credit responsibly can expect their credit limits to increase over time.

Experian

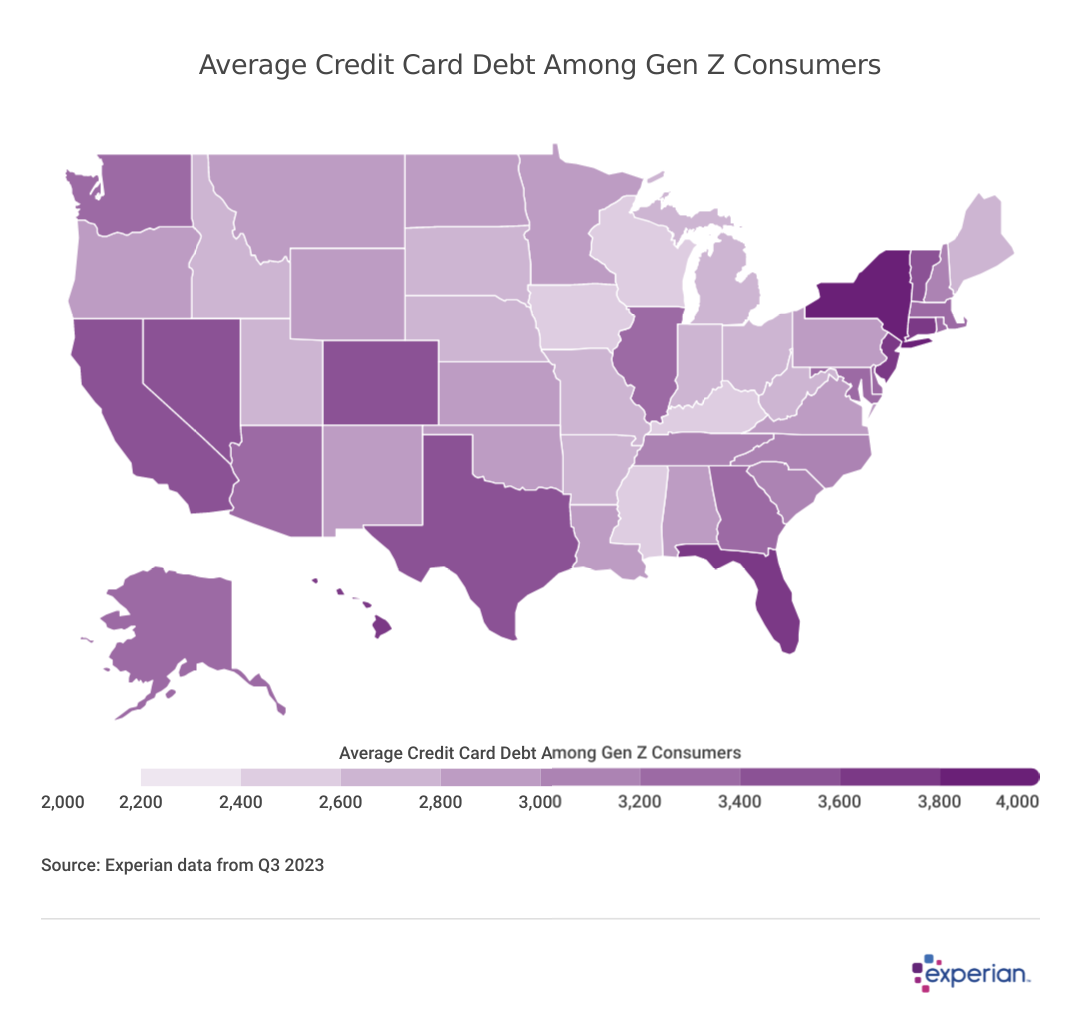

Where the Gen Z Credit Users Are Located

Heatmap showing “Average Gen Z Credit Card Debt by State”.

Gen Zers in the more populous states of California, New York and Texas carry higher credit card balances than others. And as rent continues to rise, it’s taking a larger bite of take-home income.

Experian

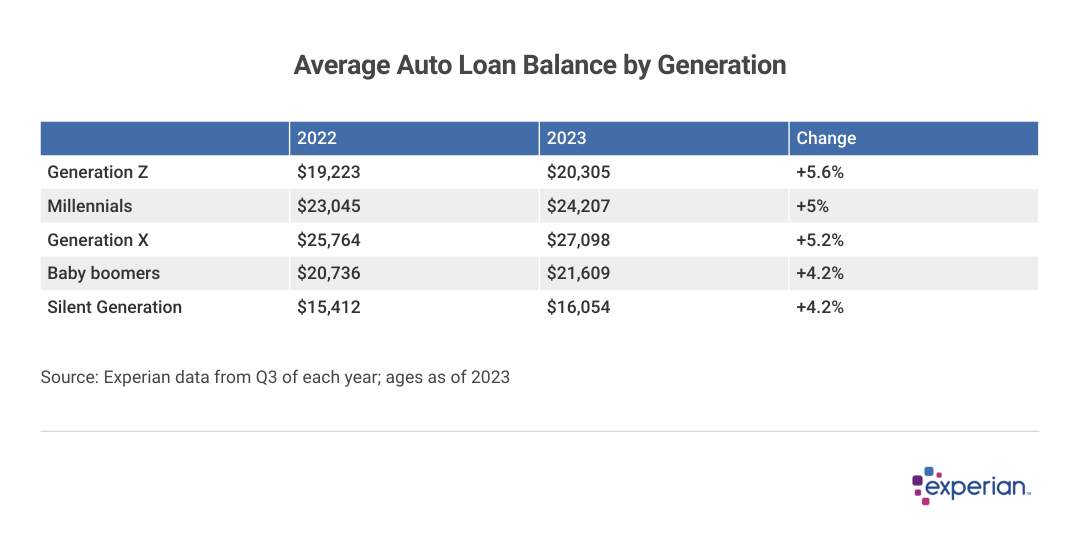

Gen Z Drivers Carry an Average Auto Loan Balance of $20,305

Table showing “Average Auto Loan Balance by Generation”.

At least drivers have more selection in choosing their ride, as used car prices are falling, inventory levels are mostly back to normal, and dealers are offering incentives like low-cost financing for some new models.

A glance in the rear-view mirror, however, shows that car loans recently made are costing consumers more across the board. Car prices, and the cost of the attendant car loans often used to purchase vehicles, have still increased for all consumers in the past year, more or less equally across all generations.

Generation Z will need all the savings they can get, however, as auto insurance premiums continue to skyrocket. Insurance rates climbed more than 22% in the past year, according to U.S. Bureau of Labor Statistics data, and inexperienced younger drivers are generally the costliest to insure.

Experian

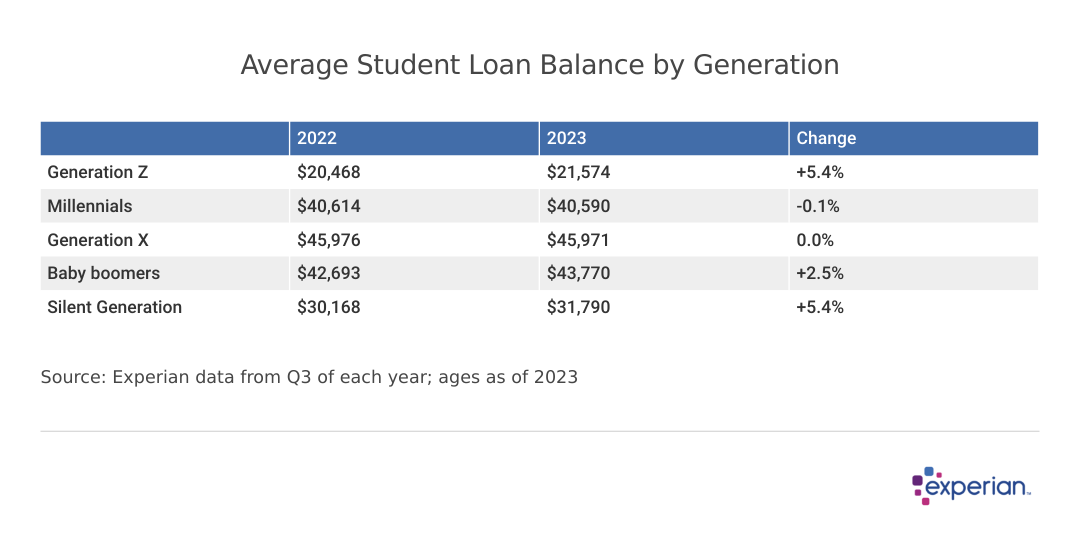

Gen Z’s Average Student Loan Balance of $21,468 Will Likely Rise

Table showing “Average Student Loan Balance by Generation”.

Although more members of Generation Z are pursuing the trades, more than half of Gen Z have entered the realm of higher education, according to Pew Research data. And compared with other generations, Generation Z student debt is much smaller thus far. That will change in the upcoming years, as some continue advanced degree studies, a more costly education than pursuing an undergraduate degree.

Most Gen Z borrowers planning to pursue advanced degrees have yet to enter a program or complete their graduate studies. Graduate-level education is often more expensive and can result in more student loan debt than undergraduate education, with borrowers typically not on track to begin to repay until their late 20s or early 30s.

While the average student loan balances of Generation Z are expected to increase in the future, these consumers will have more tools to manage monthly payments from the very start of their repayments, unlike other generations before them. Once fully implemented, it’s expected that a combination of income-based repayment plans and loan forgiveness programs for public service will help ease the burdens of education debt.

Generation Z Embraces Buy Now, Pay Later

The way consumers spend their hard-earned money is changing for everyone, not just for Generation Z. (When’s the last time you wrote a check?) However, Gen Z is more keen than others to embrace electronic payments as well as new types of alternative credit that’s been cracked open by technological advances like buy now, pay later (BNPL) plans.

Generation Z is associated the most with BNPL, but their older brothers and sisters may be catching up. According to alternative credit provider Afterpay, three-quarters of both Gen Zers and millennials reported using buy now, pay later in the past month, versus only about half of Generation X.

Experian

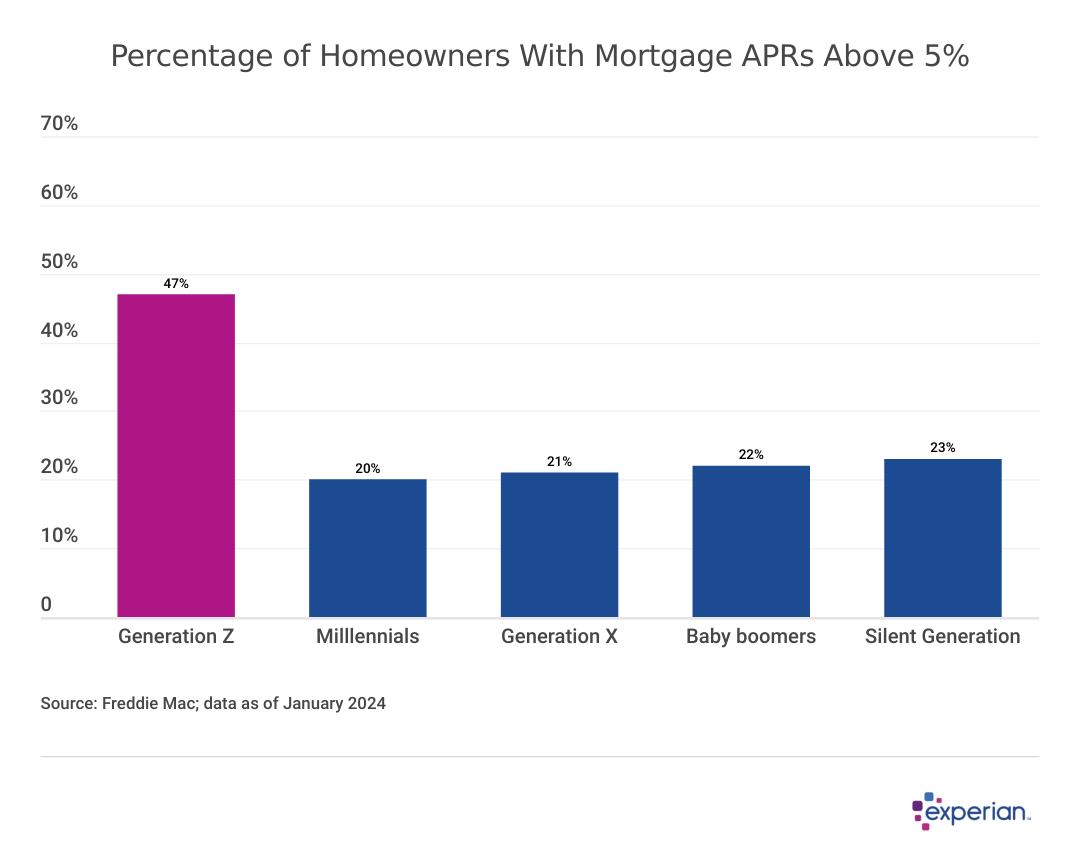

Gen Z’s Bumpy Path to Homeownership

Image of graph showing “Percentage of Homeowners With Mortgage APRs Above 5%”.

Although some among the youngest consumer generation have bought a home of their own in the past couple years, mortgage payments are as high for them as they are for older recent homebuyers who likely have more discretionary income.

More likely, they rent. Some 70% of all rental households are millennials or Gen Z, according to Experian’s State of the U.S. Rental market report. Rental prices—where most young people first begin their financial journeys—are still increasing faster than the rate of overall inflation in most markets. One consequence: More young adults live with their parents or others (roommates) than they did 30 years ago, according to data collected by the Urban Institute.

As for Gen Z homeowners, many are facing additional challenges relative to other homeowners: higher borrowing costs. Nearly half are paying more than 5% annually in interest. Besides the larger monthly mortgage payments this implies, it also means that equity accumulates more slowly for these homeowners than others.

There is an upside, though. If mortgage rates fall far enough, there will be a ready-made market of Gen Zers willing to refinance their mortgages, activity that’s barely occurring today.

While mortgage rates and few homes to choose from are placing homeownership out of reach for many, regardless of age, reporting rental payments to credit bureaus could help a renter’s credit score in the meantime. As Generation Z are the generation most likely to rent, as well as most likely in need to thicken their credit file and potentially improve their credit score, having rents reported to credit bureaus is perhaps more important for those just starting on their financial journeys. Alas, adoption among property owners has been slow, and smaller landlords may not be as likely to report on time payments to credit bureaus.

If there’s one myth to bust about young people, it’s that they’re forever optimistic. According to a survey recently published by consultancy Deloitte, more than half of Gen Z report living paycheck to paycheck, and only 1 in 3 say the overall economic and social situation will improve in the coming year—a polite way of saying most don’t think things are getting better anytime soon.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.