How to find the right business gas credit card in 2026

Jose Miguel Sanchez // Shutterstock

A gas credit card is a type of business credit card that provides benefits specifically for fuel-related expenses. These cards offer rewards, discounts, or cash back on fuel purchases, turning routine spending into meaningful savings for companies that rely on vehicles. Some cards offer flat-rate rewards at gas stations, while others give higher returns within certain networks or spending categories.

Whether you’re running a delivery fleet, managing field service teams, or building a new business, the right gas credit card transforms unavoidable fuel costs into profit opportunities while giving you complete spending control.

In this guide, Ramp compared the top business gas, fleet, and fuel cards by rewards, savings, and control features—so you can quickly find the right fit for how your business fuels and operates.

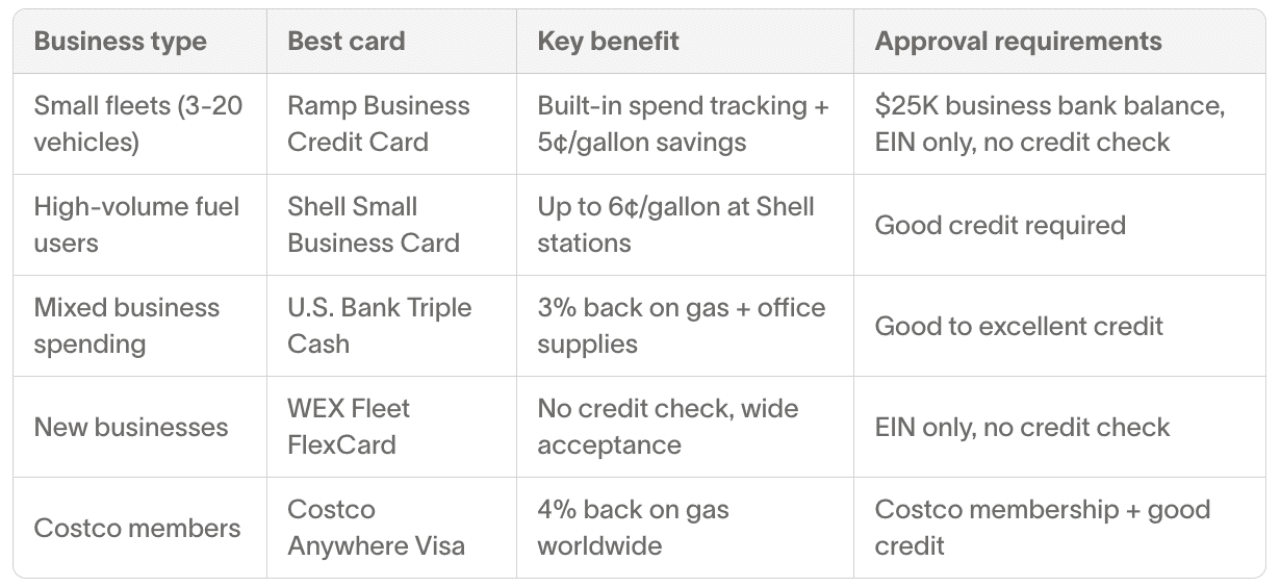

Summary: Best business gas credit cards by business type

Ramp

Understanding different types of business gas cards

A company gas card—also known as a fleet gas card—allows employees to pay for fuel in company vehicles without using personal funds. These cards help track spending and remove the need for cash or reimbursement. Some advanced options even collect odometer readings and fuel usage data to improve efficiency and provide detailed analytics.

The most common types include fuel credit cards and prepaid cards. Credit-based fuel cards typically offer better reporting tools, higher limits, and help build business credit, while prepaid cards require loading funds in advance but don’t require credit checks. Fuel credit cards are ideal for established businesses that want stronger oversight and the ability to earn rewards or cash back on every purchase.

Fleet cards, such as WEX, are designed specifically for companies that manage multiple vehicles and need features like driver IDs, per-transaction limits, and custom reporting. Business gas credit cards offer similar control benefits while also earning rewards across other spending categories.

If your goal is to maximize rewards, choose a business gas credit card. If your priority is tighter spend control and detailed reporting, a fleet card may be the better option.

Why your business needs a dedicated gas credit card

If your business spends more than $500 monthly on fuel, you’re losing money and control without a dedicated gas card. Here’s what the best business gas credit cards solve:

Immediate cost control:

- Stop fuel theft and misuse with purchase restrictions and real-time alerts

- Eliminate receipt hunting with automated expense tracking

- Reduce fuel costs by 3-6¢ per gallon through rewards and discounts

- Simplify tax prep with categorized fuel expenses

Long-term benefits of business gas cards:

- Build business credit separate from personal finances

- Professional appearance when employees use company cards

- Cash flow management with payment terms and credit lines

- Scalable expense controls as your team grows

Unlike general business credit cards, gas cards are built specifically for fuel oversight, giving you deeper control over how, where, and when employees spend. Many let you set limits by driver or vehicle, restrict purchases to fuel or maintenance categories, and track usage across teams or job sites.

They also generate detailed spend reports, automate receipt matching, and simplify cost allocation by department or project. Many offer cashback or per-gallon discounts and are accepted nationwide—ideal for teams operating across regions.

If your business is scaling or manages frequent travel, a dedicated gas card helps turn recurring fuel expenses into predictable, trackable savings.

Fleet cards vs. business gas credit cards

Not all fuel cards work the same way. Both fleet cards and business gas credit cards help manage fuel costs, but each serves a different type of business.

Fleet cards are built for companies operating multiple vehicles or field teams. They often provide per-gallon discounts and oversight features such as driver IDs, mileage tracking, and purchase limits. Many include reporting tools that help monitor fuel efficiency, prevent misuse, and centralize spending data in one place.

Business gas credit cards function like traditional business credit cards but with elevated rewards on fuel purchases. They’re accepted almost everywhere and frequently offer cash back on other categories, such as dining or office supplies. These cards are a strong fit for smaller teams or organizations that don’t need detailed fleet-level reporting.

Prepaid or secured cards can also support newer businesses that want to manage spending while establishing credit. They’re easier to qualify for but usually don’t include rewards or advanced tracking features.

In short, fleet cards offer deeper visibility and control, while business gas credit cards provide broader acceptance and flexible rewards.

How to choose the right business gas card for your needs

The best gas card for your business depends on more than just rewards. It should align with how your team fuels, how you manage spending, and what features actually save time. Here’s what to consider:

Control and track fleet spending (Best for businesses with 5+ vehicles)

If you’re losing money because you can’t see where your fuel budget is going, you need a card built for oversight and control. Prioritize cards with real-time alerts, product-level restrictions, and detailed reporting tools.

Maximize rewards on necessary spending (Best for consistent fuel users)

Businesses that view fuel as an unavoidable expense should turn those costs into profit through cashback and rewards. Look for high reward rates, simple redemption, and no annual fees. The Costco Anywhere card offers 4% cashback, while the U.S. Bank Triple Cash provides 3%, turning everyday fuel spend into real savings.

Establish business credit and legitimacy (Best for new businesses)

New business owners often need payment tools that help build business credit while projecting a professional image. Prioritize gas credit cards with business credit reporting, EIN-only approval processes, and no personal guarantee requirements. Various secured business credit cards help establish creditworthiness while providing essential expense management capabilities.

Simplify operations and reduce admin (Best for time-strapped owners)

For teams that want fuel expenses to manage themselves, automation is key. Choose cards with automatic expense categorization, accounting integrations, and comprehensive mobile apps.

Security features to consider:

- Real-time transaction alerts and pump-only limits

- Driver ID verification or odometer tracking

- Location-based restrictions to prevent misuse

Are fuel cards worth it for small businesses?

Yes, fuel cards can reduce administrative work for small businesses by automatically tracking and categorizing every purchase, eliminating the need for manual receipt collection and reimbursements. Combined with fuel discounts and rewards that can reduce costs by 3–6¢ per gallon, they often deliver savings that outweigh any fees or effort required.

For businesses spending $500+ monthly on fuel, the operational efficiency and cost savings make fuel cards a clear improvement. And for growing businesses, the ability to set spending limits and monitor purchases in real time helps maintain cash flow discipline.

How to start applying for a business gas card

Once you’ve identified the card that fits your fuel needs, oversight requirements, and budget, the next step is applying.

Here’s what the process typically looks like:

- Eligibility check: Most cards require a valid EIN and basic business information. Many also require a personal credit check or personal guarantee; some EIN-only options review business financials such as cash flow or bank balances instead of personal credit.

- Online application: When applying for a business credit card, you’ll be asked to provide your legal business name, EIN, contact details, and business bank account information. Some issuers may also request ownership or entity details.

- Approval and setup: If approved, activate the card online or by phone, then configure spending limits, categories, and employee cards as needed. Connect accounting integrations if your provider supports them.

- Start using your card: Begin fueling and tracking expenses. Most gas and fleet cards include real-time monitoring, receipt capture, and fuel-only controls, which is especially helpful for teams with multiple vehicles or drivers.

Are there any easy-approval business gas cards available?

Yes, some types of business gas cards, such as prepaid cards or select fintech-backed options, are easier to qualify for and may not require a personal credit check. However, most traditional business gas cards do require a credit check and/or personal guarantee.

Here’s a breakdown of the most common types of easy-approval business gas cards, and how to tell which one fits your needs:

1. Prepaid fuel cards

Prepaid gas cards don’t require a credit check because you load funds onto the card in advance. They’re a simple way to manage fuel spend if your business is new, has limited credit history, or wants to avoid debt entirely. That said, prepaid cards usually don’t offer rewards or credit-building benefits, and some have limited acceptance depending on the gas station network.

Best for: Businesses that want basic spend control but don’t need to build credit.

2. Secured business credit cards

Secured cards require a cash deposit up front and are typically used to build or rebuild credit. While not all are fuel-specific, some secured business credit cards offer modest cashback on gas purchases. These cards are better suited for long-term credit growth than short-term savings or fleet-wide fuel management.

Best for: Businesses with moderate fuel needs that want to build business credit over time.

3. Business charge cards with alternative approval

Some business gas cards use alternative underwriting. Instead of relying on personal credit, they evaluate business financials like bank balance, cash flow, or revenue. These cards work well if you have strong business activity but limited credit history.

Most businesses don’t overspend on gas because they’re fueling too often. They overspend because:

- They lack visibility into who’s buying what, where, and when

- They can’t enforce policies or set limits in real time

- Reconciling receipts is messy and time-consuming

- They’re using a rewards card built for consumers, not companies

These aren’t credit card problems—they’re operational ones. And the right gas card should solve them.

This story was produced by Ramp and reviewed and distributed by Stacker.

![]()