Credit card balances are growing fastest in these 20 cities

Jacob Boomsma // Shutterstock

Credit card balances are growing fastest in these 20 cities

Aerial view of Fresno city skyline in California.

Consumer spending habits are an important measure of economic activity, but these trends are not necessarily in lockstep nationwide. One way to observe where consumers are spending more than they did last year is by looking at their debt. This includes their credit card balances as well as the total amount of minimum monthly payments they’re expected to pay on loans such as mortgages, credit cards, personal loans, auto notes, student loans, and more.

![]()

Experian

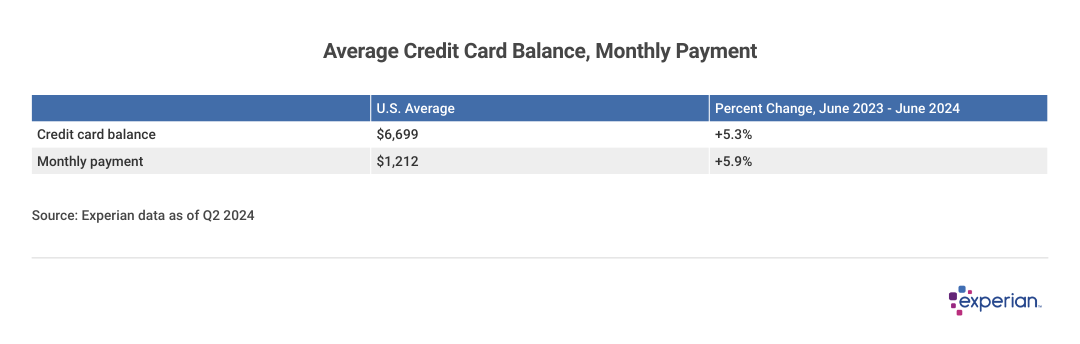

Credit Card Usage and Payment Increases in Certain U.S. Metros

Average Credit Card Balance by Monthly Payment

Experian looked at nearly 400 metros in the U.S. to observe where increases for credit cards and monthly payments were greatest over the past 12 months, through the second quarter (Q2) of 2024.

Experian

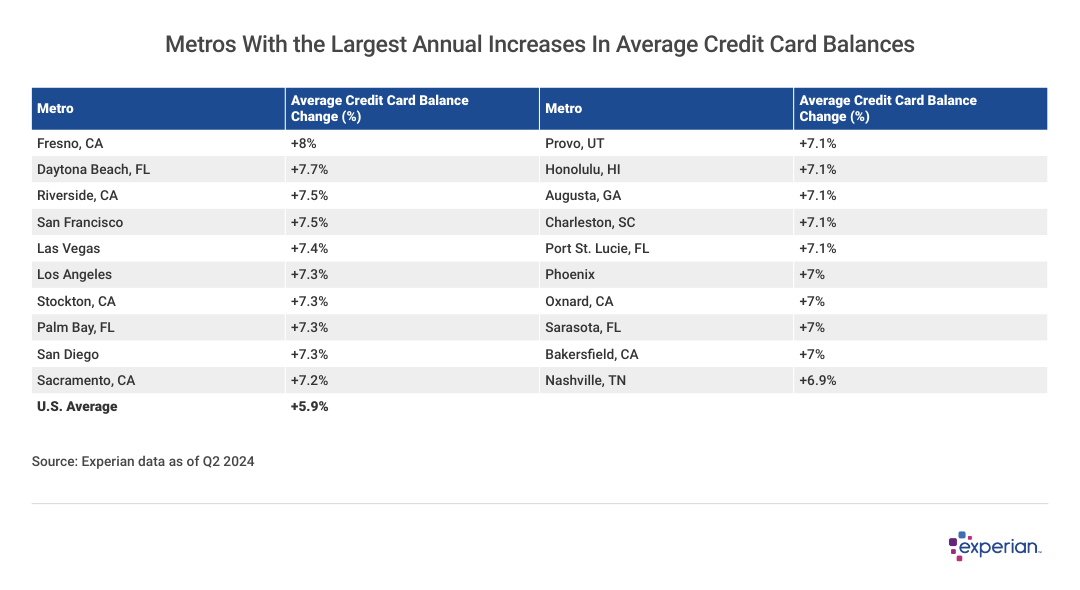

Credit Cards: The West Leads the Charge

Table listing the “Metros With the Largest Annual Increases In Average Credit Card Balances”.

Despite credit card balances growing more slowly in 2024 than in recent years, there are still outsized credit card balance increases in many metros of the southwestern U.S. as well as select Florida metros.

One phenomenon that might help explain why so many of the spendy cities are in the U.S. southwest and Florida is the increase in property insurance premiums. In the case of many Florida communities, add the cost to address deferred maintenance on many condominiums, which has recently been required by state and local ordinances.

While many consumers in these areas probably aren’t directly putting their home insurance premium purchases on a credit card, those increases can add thousands of dollars to their yearly expenses, pushing some of them to buy more goods and services with credit. With credit card APRs that now average nearly 23% in the mix, it becomes clear how shifting budgets outside of typical credit card purchases can nonetheless swell credit card balance levels.

Experian

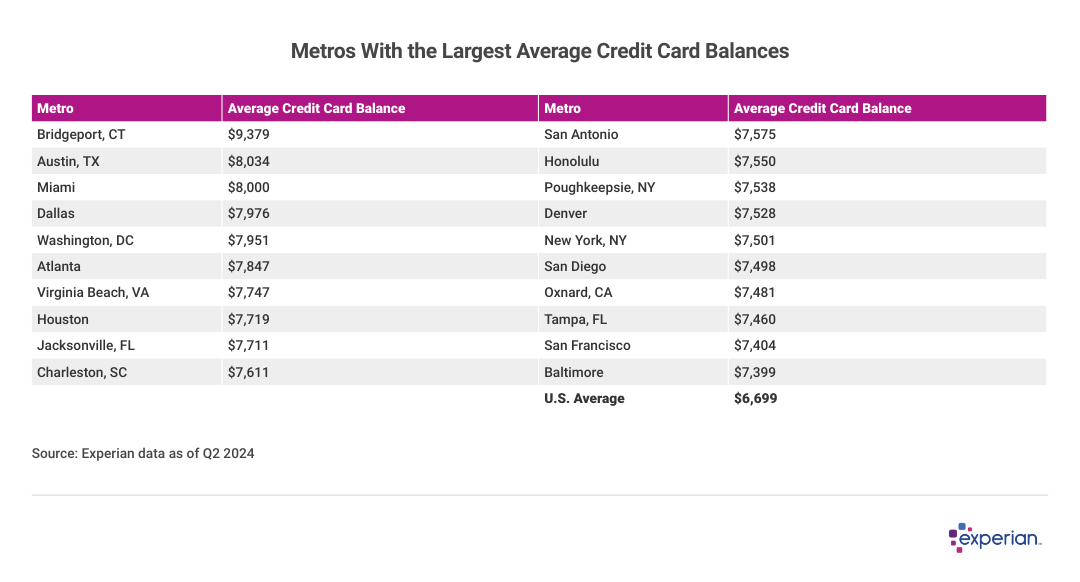

Big Cities, Big Credit Card Balances

Table listing the “Metros With the Largest Average Credit Card Balances”.

The story isn’t as complicated when identifying the metros in the U.S. where consumers carry the largest balances: In most cases, it’s a function of higher incomes and costs in these overwhelmingly large metros (despite being led by the smaller, tony bedroom communities surrounding less-tony Bridgeport, Connecticut).

Comparing the list of the top 20 metros with the cost of living in each shows that 15 of the 20 metros have costs of living above the national average. Only three cities in Texas (Dallas, Houston, and San Antonio); Jacksonville, Florida; and Virginia Beach, Virginia, have costs of living slightly lower than the national average. However, they do have other costly challenges, including higher prices for storm insurance along the Atlantic coast and, in the case of Texas, first-in-the-nation costs for automobile debt payments.

Monthly Payments Growing Even Faster in 2024, Despite Overall Inflation Subsiding

Think of monthly payments as debt repayments consumers owe their financial creditors each month. The emphasis is credit: Monthly bills for utilities and streaming services aren’t included in the calculation.

The monthly payment amount in this analysis is the sum total of the various repayments a consumer owes to creditors each month in the form of:

- Minimum payments on credit card balances

- Auto loan or lease payments

- Mortgage or home equity loan payment

- Student loans

- Personal loans

When sorting for metros where monthly payments have grown the most, Experian found 20 metros south of the Mason-Dixon line. Breaking down the list further: Eight of the 20 metros are in Florida, while another five are among the giant California metros.

But it’s some of the outliers here that are especially noteworthy. McAllen, Texas, for example, has significantly lower income levels than San Francisco, Seattle, and even Oklahoma City, yet residents there have seen their monthly payments increase as swiftly as in metro areas where incomes are on the rise.

The increases in monthly payments in these cities, ranging from 7.5% to as much as 10.6% higher in 2024 than in 2023, is more than double the inflation rate of 3% over that same period. No wonder many consumers still believe inflation is raging, despite inflation rates returning to pre-pandemic levels.

Experian

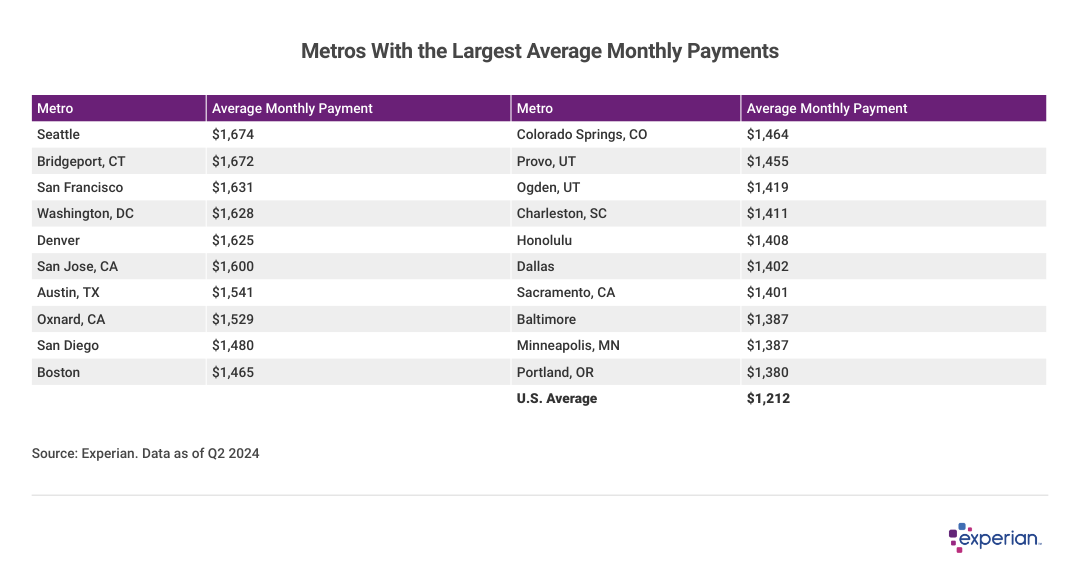

Largest Monthly Payments in Larger, More Educated Metros

Table listing the “Metros With the Largest Annual Increases In Average Monthly Payments”.

When identifying metros with the largest average monthly payments, it’s back to familiar territory—higher-priced, higher-income metros generally sport higher monthly payments than the national average.

There’s a wrinkle, however: Monthly payments include student loans. As student loan repayments resumed last September, those metros with more recent graduates among the population were more likely to see their averages climb more than other locales.

Hence the appearance of research hubs like Boston, Minneapolis, and exurban Salt Lake City metros appearing among those with the highest average monthly payments in the nation.

Other cities with top 20 monthly payments are more familiar, as more than half of these cities are also among the cities with the highest credit card balances, as previously discussed.

Experian

The Bottom Line

Table listing the “Metros With the Largest Average Monthly Payments”.

Consumers living in metros with historically higher costs of living, as well as those experiencing recent price shocks in property insurance premiums, are enduring increased monthly financial obligations, as measured by the annual percentage increase in credit card balances and total monthly payments.

In metros where real income is high and growing higher, consumers can more easily support these debt levels. However, in cases where incomes are low and or growing more slowly, rising debt levels can be an expression of increased levels of consumer stress.

Finally, recent resumptions of student loan repayments in September 2023 mean that average debt obligation levels may have increased more sharply in communities with higher than average levels of student loan borrowers.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database, which may include use of the FICO® Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.