Why car insurance companies are leaving some states

Canva

Why car insurance companies are leaving some states

A severed tree branch fallen on a silver sedan causing damage

Since the beginning of 2023, several major insurance companies have announced that they would stop writing policies or drastically reducing offerings in two of the three most populous states in the U.S. Industry heavyweights such as Geico, Progressive, and Farmers have started leaving the California and Florida auto insurance markets, citing rising coverage costs and other changing market factors as the reasons for doing so.

Insurance regulators in both states have expressed concerns about the impact that a dwindling market could have on drivers. They’ve also voiced a looming fear that such moves could mark the start of a trend that spreads to other insurers – and other parts of the country.

Automoblog breaks down the complex conflation of causes and potential effects of these developments.

Several major insurers are leaving California and Florida

In January, major news outlets reported that some of the country’s biggest insurance companies were effectively pulling out of the California market. According to one CBS News story, Progressive had stopped advertising in the state and Geico had closed its California offices. The article quoted an insurance broker who said that State Farm was only offering quotes in person, and not over the phone.

Then, in July, news broke that Farmers Insurance was going to stop offering auto coverage and other insurance policies in the state of Florida. The company only accounts for 2% of the total Florida auto insurance market, and it said that it would continue to offer policies through subsidiaries such as Bristol West and Foremost Signature.

Nonetheless, the announcement prompted Florida Insurance Commissioner Michael Yaworsky to write an official letter to Farmers, underlining the significance of the company’s exit.

“Florida’s leaders have stepped up to the plate by delivering historic reforms to Florida’s property insurance market to ensure competitiveness and increase consumer choice,” said Yaworsky, referring to legislative actions taken earlier this year. “We are disappointed by the hastiness in this decision and troubled by how this decision may have cascading impacts to policyholders.”

Myriad factors have created a difficult situation for insurers

According to the insurance companies and organizations such as the American Property Casualty Insurance Association, the reason for these exits is simple mathematics. According to the APCIA, auto insurance losses increased at a rate of 25% while insurance premiums only went up by 4.5%.

Automoblog spoke to APCIA Department Vice President of Personal Lines Robert Passmore about these developments. He said that the difference in these increases has made it financially difficult for companies to continue to insure drivers in many cases.

“Nationally, rapid increases in overall economic inflation continue to drive up auto insurance losses,” said Passmore. “Insurance claims inflation has continued to rise faster than the underlying consumer price index, far outpacing increases in premiums.”

However, the cause of these price increases is more complex. Several factors have contributed to rapid growth in the cost of paying out insurance claims.

![]()

Automoblog

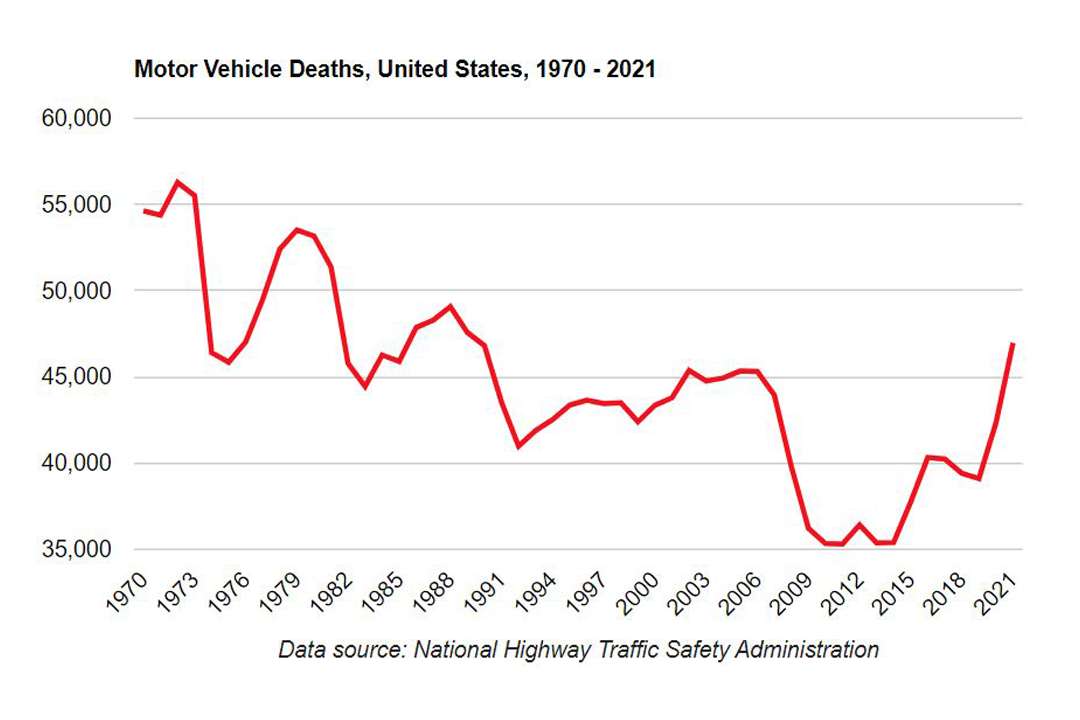

The rate and severity of auto accidents is on the rise

A graph showing the number of motor vehicle deaths since 1970

One of the major drivers in the increase in claims costs is that car accidents have become more frequent and more severe in the last few years. According to the National Safety Council (NSC), 2021 marked the second year in a row that motor vehicle deaths increased. The U.S. saw an 11% increase in traffic fatalities in 2021 after an 8.3% increase in 2020.

These increases mean that auto insurers are paying out more claims by number than in previous years. It also means that the average payout for individual claims increased over this period.

Automoblog

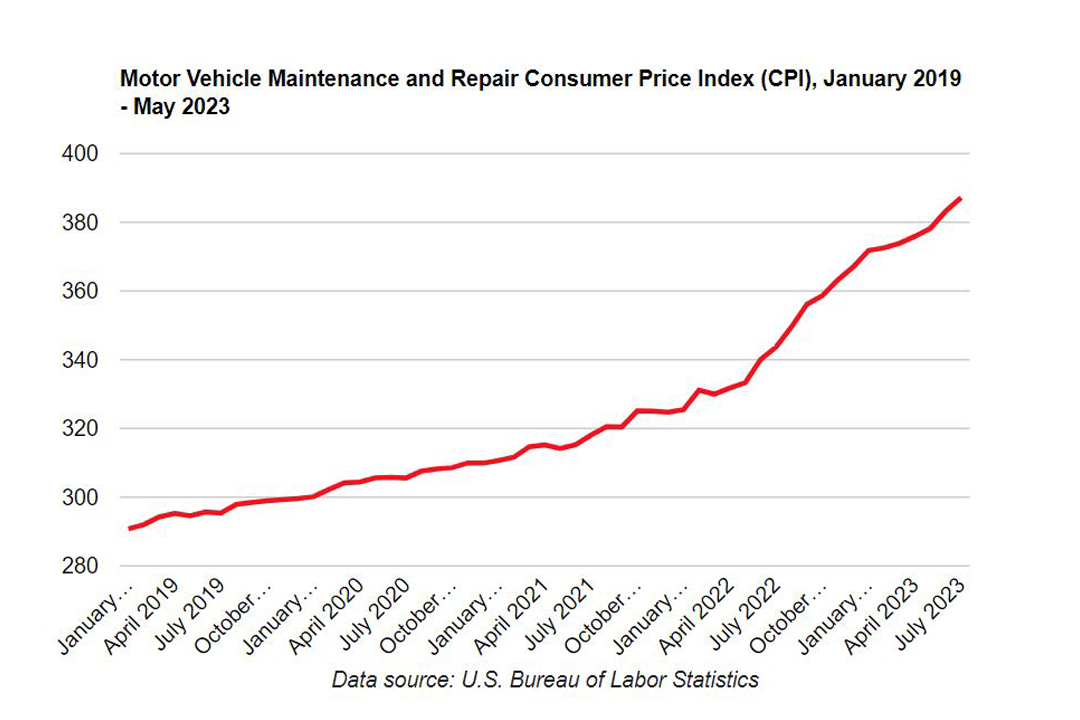

Auto repairs are becoming more expensive

A graph showing the consumer price index cost of automobile repair and maintenance in the US since 2019

In addition to traffic accidents becoming more frequent and more catastrophic, the cost of making repairs to damaged vehicles has also increased. According to data from the U.S. Bureau of Labor Statistics (BLS), the consumer price index (CPI) of auto repairs and maintenance increased by 33.2% between January 2019 and July 2023.

As a result, payouts for individual repair claims have increased substantially compared to the same repair services just a few years before. Even if the rate and severity of auto accidents had remained static, claims costs would still have gone up.

Automoblog

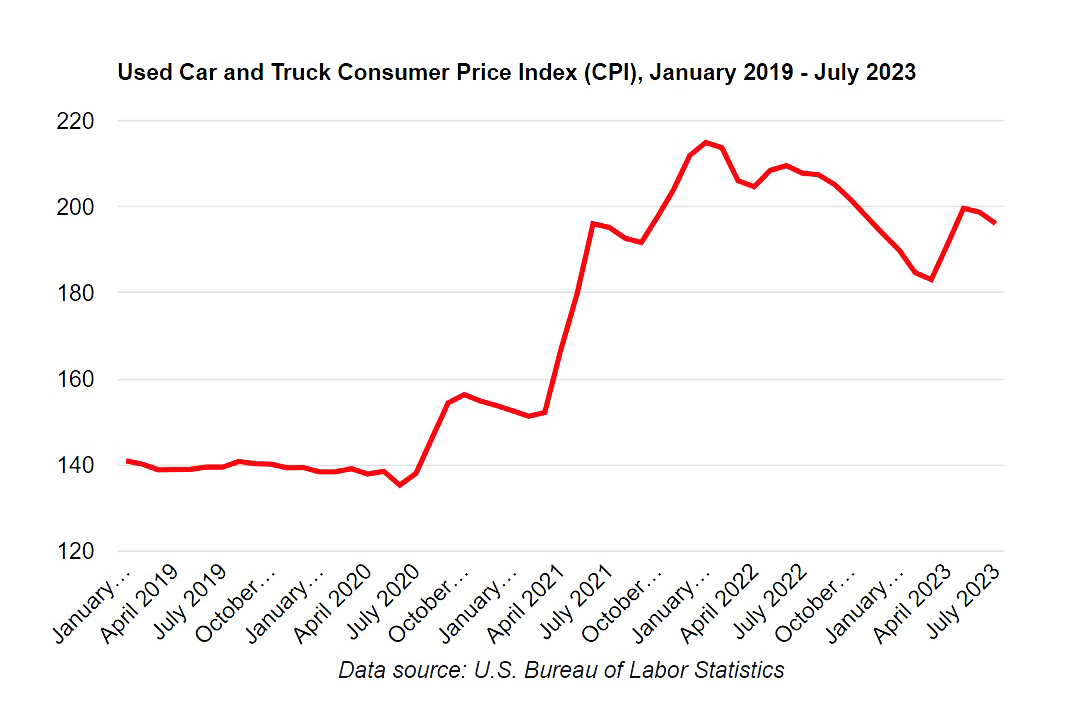

The high price of used cars has increased replacement costs

A graph showing the used car and truck consumer price index from 2019 to 2023

Despite leveling off somewhat in recent months, used car prices are still at or near all-time highs after a dramatic climb. According to BLS data, the CPI for used cars and trucks has increased 39% since January 2019.

For customers who have collision and comprehensive insurance policies, insurers often pay current market value for total loss claims. With the significant increase in used car prices, auto insurance companies have had to pay out much more for totaled vehicles – in many cases, for vehicles with premiums based on cars valued lower at the start of the policy than when the claim was made.

Catastrophic climate events are becoming increasingly common

Climate change has also changed the math for insurers. Events such as wildfires in California and hurricanes and floods in Florida have increased the number and severity of claims in the states.

In this case, the home insurance market has seen much of the increase in climate-related payouts. However, since most major insurers offer home and auto insurance among other products, the increase in costs in one category still affects the company’s bottom line and therefore, the ability to make money in a given market.

Some say regulations have made it difficult for insurers to respond

Another contributing factor is government regulations that, according to the insurance industry, make it hard for insurers to adjust to changing risks. In California, for example, insurance companies must get permission from the state’s insurance commission to increase rates. Some insurers in the state haven’t been given permission to increase rates in more than three years, despite the aforementioned increase in financial risk.

“The collision-to-loss ratio in California is now up to 88.6 percent and the comprehensive loss ratio in California is up to 173.9 percent,” said Passmore. “That means for each dollar insurers take in for comprehensive coverage, they are paying out $1.73. Unfortunately, due to an antiquated regulatory system in California, insurers have been unable to nimbly respond to urgent situations like inflation. This means insurers are not able to get the rates they need to keep up with inflation and higher accident severity.”

A spokesperson for the California Department of Insurance (CDI) offered reporters a different perspective, saying, “while insurance companies are focused on increasing rates, the Department of Insurance is focused on protecting drivers and helping them get the most value from the premiums they pay.”

The trend could get worse, increasing costs for drivers

While the tension between insurance companies and state regulators in California and Florida continues to grow, drivers in the states have started to see their options dwindle and their costs increase. In Florida, drivers pay an average of 30.4% more than they did just a year ago, in 2022. California drivers have seen a cost increase of only 4%, largely due to state regulatory policies.

These cost increases have been, in part, due to the rising costs for insurers. However, a reduced number of carriers in a market means less competition and less incentive for companies to offer competitive rates. Since the announcements were made this year, the exit of major insurers has likely not had an impact on costs just yet. But if left unchecked, the situation could soon translate into higher costs and reduced choice for car owners.

Government agencies and insurance companies have, however, started to attempt to make changes that could alleviate the issue. In California, some insurers are asking the CDI for permission to raise premiums – ostensibly to allow them to continue to operate in the state. State Farm, Allstate, and Farmers have requested a 7% increase, while Progressive has asked the agency to increase its rates by more than 19%.

In Florida, the state legislature was already in the process of passing legislation to try to stabilize the insurance market. Part of that legislation has been directed at curbing a wave of lawsuits against insurers in what the insurance industry views as abuses of the legal system. Florida officials have said that legislative action also works to protect insurance customers.

Passmore expressed optimism over the legal developments in Florida, but said changes won’t have an immediate impact.

“Just over the last year, Governor DeSantis and Florida’s legislative leaders passed important legal reforms to protect consumers and restabilize the insurance market,” he said. “It will take time for the current wave of legal system abuse to wash through the system, but the new reforms have created a strong foundation for the future.”

Some of the trends that have led to the current situation could slow down or even reverse in the coming years. It’s possible that the increase in the number and severity of traffic accidents is a temporary trend. If inflation continues to cool down, costs could also start to normalize for insurers. And if supply chain issues such as the semiconductor shortage start to improve, the country could also see car prices start to come back down.

However, the threat and impact of climate-related events are, by almost all predictions, likely to continue to worsen in the near and distant future. In the big picture, rising insurance costs may be a relatively minor issue when facing a global climate crisis, but it’s one that has an immediate and significant impact on people and their ability to pay for legally required auto insurance.

This story was produced by Automoblog and reviewed and distributed by Stacker Media.