Credit card APRs are at an all-time high—and so are credit card providers' profits. What's behind the record-high rates?

SkunkChunk // Shutterstock

Credit card APRs are at an all-time high—and so are credit card providers’ profits. What’s behind the record-high rates?

paper bank statement showing 23.9% APR with pen in background

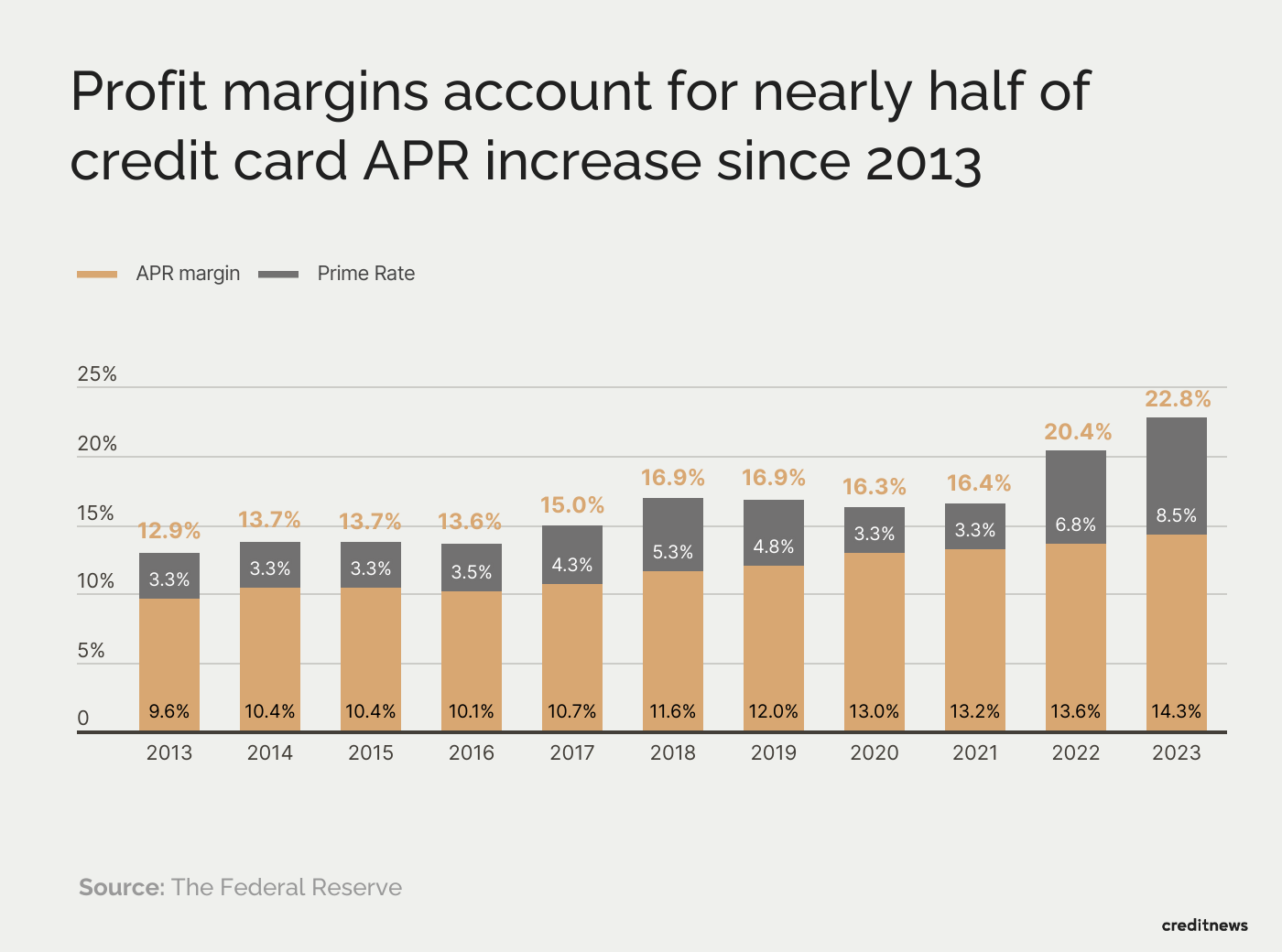

The Fed tends to take all the blame for high borrowing costs—but is the central bank really the only culprit? According to the Consumer Financial Protection Bureau (CFPB), the average credit card APR has nearly doubled over the past decade, climbing from 12.9% in 2013 to 22.8% in 2023.

The rise itself isn’t unexpected given the post-Covid-19 interest rate hikes. But what is surprising is that a lot of that increase in APRs has nothing to do with interest rates. In fact, Creditnews reveals that nearly half of the jump in credit card APRs over the past decade is a result of growing profit margins.

![]()

Creditnews

Credit card APRs continue to grow

graph showing profit margins due to APR increases

For revolving credit card accounts, the average APR margin is now a whopping 14.3%, the highest level in recent history, according to the CFPB. A separate CFPB report found that credit card issuers can charge excessively high rates simply because they don’t have enough competition.

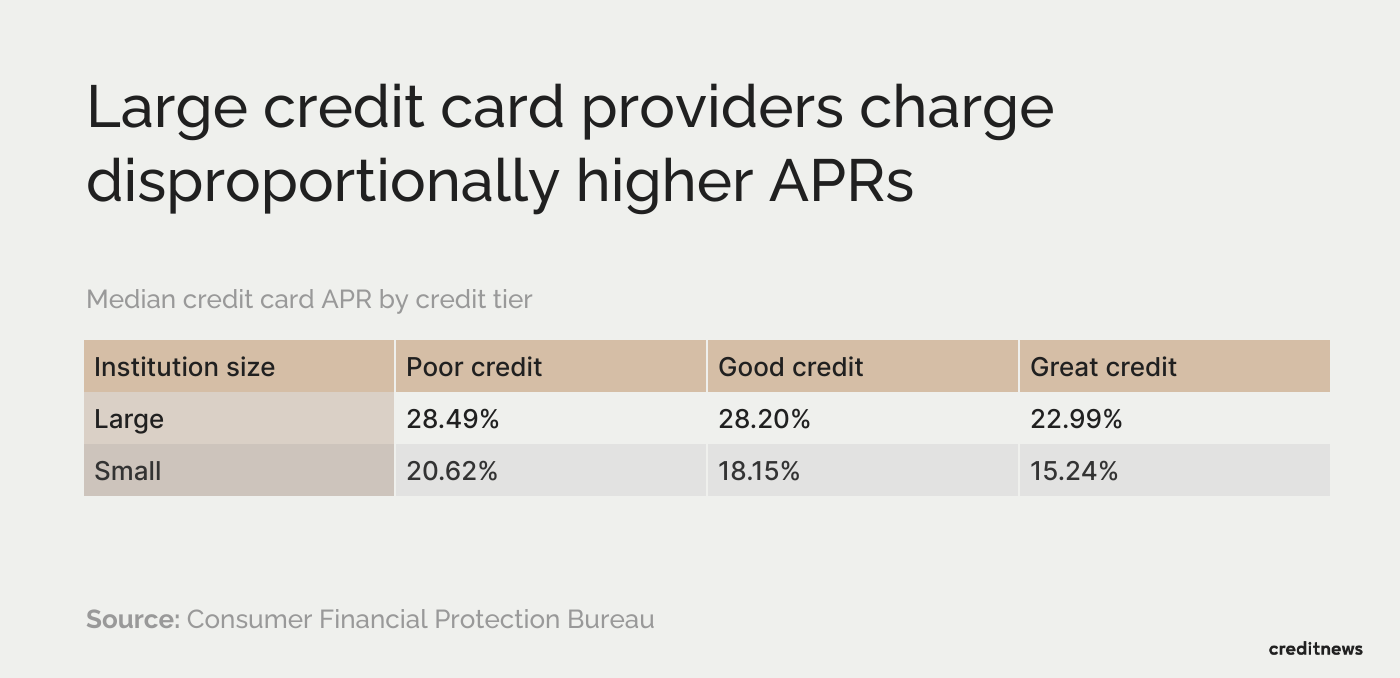

In fact, the largest 30 credit card companies account for a staggering 95% of the country’s credit card debt, with the top 10 dominating the marketplace, according to the CFPB. These large players charge APRs that are eight to ten percentage points higher than smaller banks or credit unions. That means 190 million Americans who use credit cards likely pay record-high fees not solely due to higher borrowing costs in the economy but because credit card providers have set sky-high rates favorable to their profit margins.

Unfortunately, many consumers have little choice about the rates they pay.

Creditnews

The larger the lender, the greater the APR

table showing median APR by credit tier

Not only that, nearly half of large credit card providers offer exceedingly high APRs of more than 30%. This could be fixed if smaller companies had a bigger foothold in the credit industry, according to CFPB director Rohit Chopra. “Americans would be better off with newer entrants or smaller players in the market,” he said. “For the average household, switching can actually save them hundreds and hundreds of dollars over the course of the year.”

Those savings aren’t just limited to interest payments but fees as well. According to the same CFPB report, large issuers charge an annual fee that’s roughly 70% higher than at smaller institutions. These providers employ “concerning” practices that “limit price competition, prop up rates for consumers carrying a balance, and have the potential for harm.”

America’s growing debt burden

America’s credit card debt has soared more than 40% since the height of Covid-19 in mid-2021—surpassing $1 trillion for the first time ever. A significant chunk of that debt, however, was amassed involuntarily for the most part. The combination of inflation and rising APRs trapped many Americans in so-called “persistent debt”—a situation where cardholders’ payments only cover charges for interest and fees. By the CFPB’s estimates, 1 in 10 credit card accounts are in “persistent debt.”

Meanwhile, credit reporting agency TransUnion reported that the average credit card balance reached $6,360 in Q4 2023, also a new record. “Consumers are just spending more,” according to Charlie Wise, senior vice president of global research and consulting at TransUnion. “Even though the inflation rate is down, that doesn’t mean prices are coming down.”

“Consumers are struggling with their payments,” Wise added, referring to the spike in credit card delinquencies last year.

According to TransUnion, the number of cardholders in “serious delinquency,” or more than 90 days past due, is at the highest level since 2009.

Americans on the lowest rung of earnings are more likely to bear the brunt of delinquencies. Researchers at the New York Fed reported a concerning uptick in “financial stress” among lower-income debt holders, who are “struggling in today’s post-pandemic period.”

“We see this in rising early delinquencies in auto and credit card debt,” the Fed wrote in a January 2024 report.

Meanwhile, credit card companies’ record profits show no sign of slowing.

This story was produced by Creditnews and reviewed and distributed by Stacker Media.