Non-mortgage debt balances are declining in 2024

PeopleImages.com – Yuri A // Shutterstock

Non-mortgage debt balances are declining in 2024

Couple happily discussing finances.

With the notable exception of mortgages, consumer debts are declining in 2024. This reverses a trend of larger borrowing balances among American consumers that goes back to the Great Recession.

Non-mortgage debt includes the total balance of a consumer’s loans and lines of credit when their first and second mortgages are removed from consideration. That’s obviously a large carve-out: Mortgage balances exceed $250,000 on average in 2024, and collectively make up about two-thirds of the overall consumer loan balance of around $17 trillion, according to Experian data.

But focusing on non-mortgage debt allows analysts and others to zoom in on the parts of a consumer’s financial life that change more often and apply to a broader cross section of the population. Only 40% of consumers are paying off a mortgage or other type of home loan in most given years, but around 85% have at least one credit card, and more than 62% have at least one auto loan.

![]()

Experian

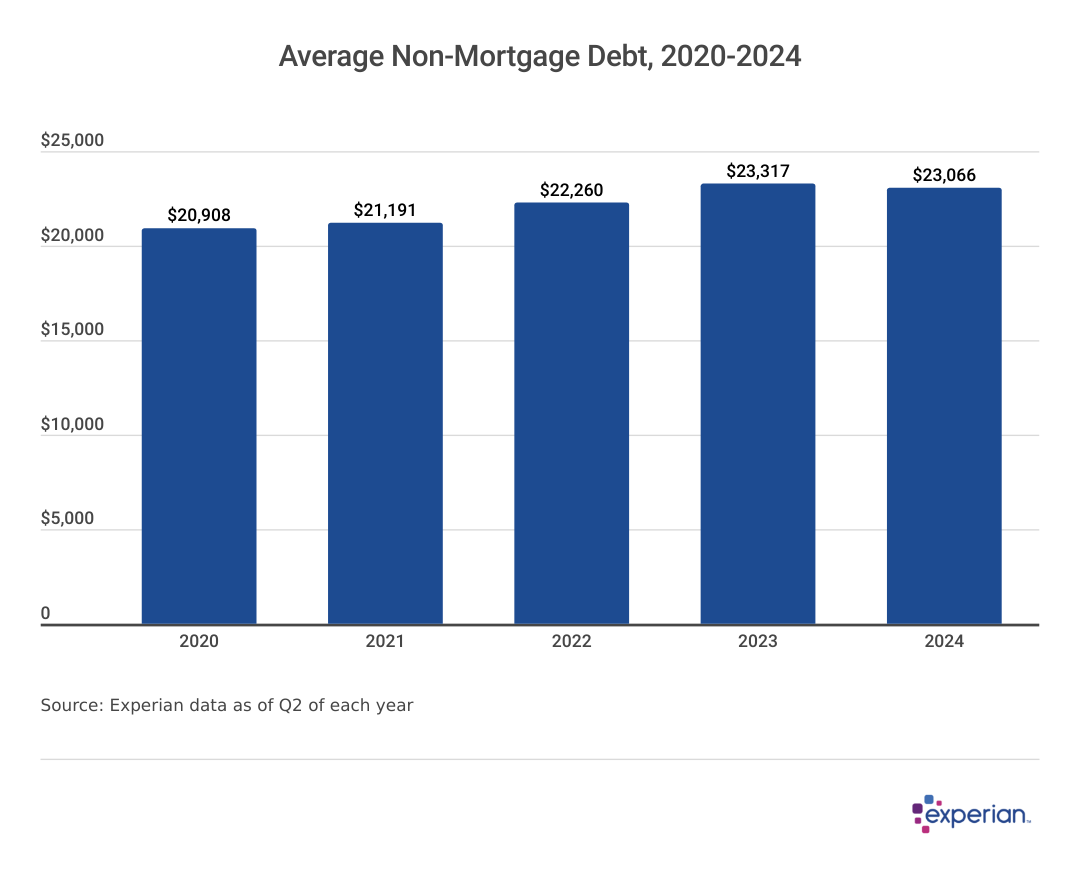

Average Debt Balances, Excluding Mortgages, Fell in 2024

Chart showing “Average Non-Mortgage Debt, 2020-2024”

In the face of a period of relatively higher rates of inflation, nationwide average loan balances (excluding mortgages) fell by 1.1% from the second quarter (Q2) of 2023 to Q2 2024, according to Experian data. That may not seem like much of a decline, but it marks a major reversal in consumer debt trends.

The average non-mortgage debt balance of $23,066 is still significantly larger than the $20,908 average in 2020. But in the face of 23% credit card APRs and near $50,000 average sticker prices for new automobiles, any reversal of the relentless upward trajectory of consumer balances is noteworthy.

Experian

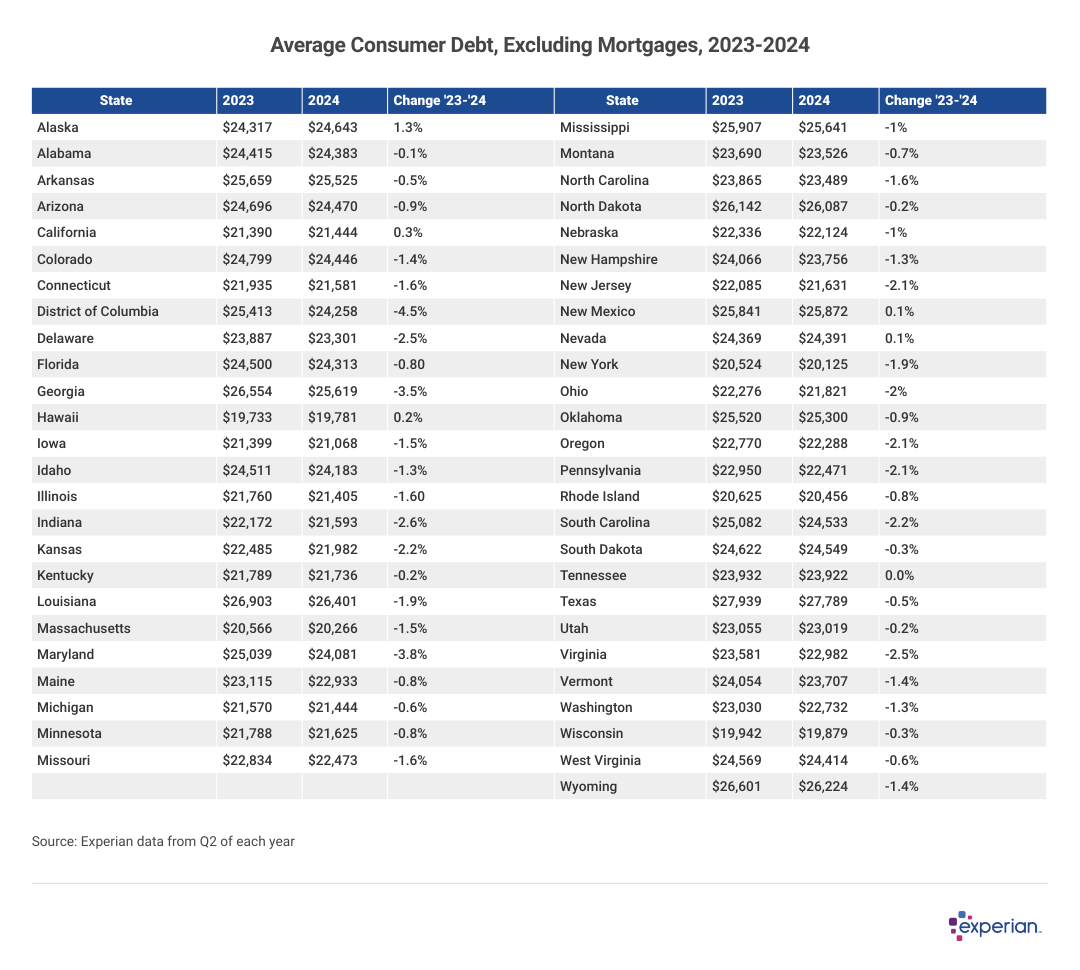

Average Non-Mortgage Debts Not Equally Distributed

Table showing “Average Consumer Debt, Excluding Mortgages, 2023-2024”

Looking at where non-mortgage balances are falling the most, some broad patterns emerge. While some regions saw their balances decline, states where inflationary costs were steeper saw less, if any, decline.

Only a handful of states, mostly in the Western region of the U.S., saw their average non-mortgage balances continue to increase this year, albeit slightly. The state where non-mortgage debt grew the most was Alaska, by 1.3% to $24,643 in 2024.

Meanwhile, states in the Northeast saw their average balances decline the most, broadly speaking. And although Washington, D.C., isn’t a state, it leads the nation in declining non-mortgage debt. Average balances there fell by 4.5% in 2024, to $24,258. Adjacent Maryland was runner-up with a 3.8% decline in average non-mortgage debt.

Canceled Debts Behind the Reversal

A main driver behind the cresting levels of non-mortgage debts is student loan cancellation. Despite the halting stops and starts in student loan payment and programs impacting student loan borrowers from 2020, some federally funded student loans have been canceled by the Department of Education. The sum total of these loan cancellations exceeded $175 billion as of fall 2024, according to the department.

Experian

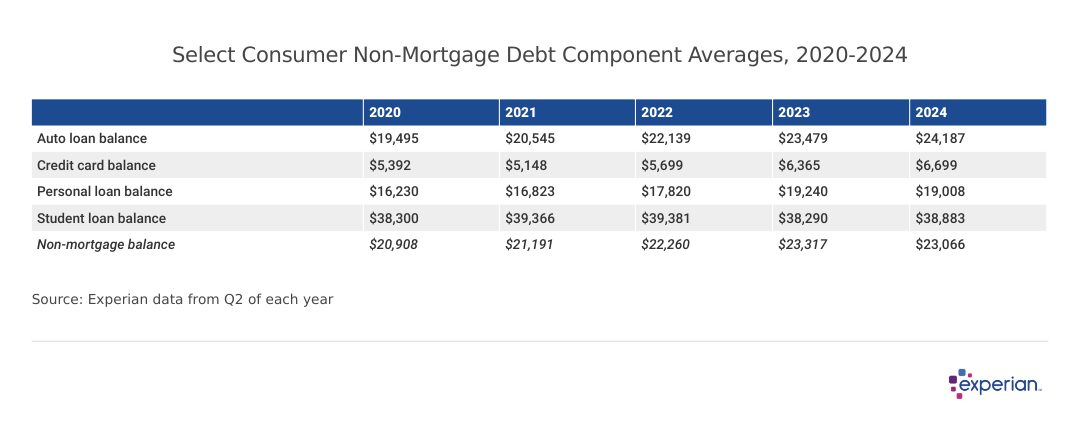

Select Consumer Non-Mortgage Debt Component Averages, 2019-2024

Table showing debt balance from 2020-2024.

Indeed, average student loan balances peaked in 2021 and 2022 at roughly $39,400 before falling by more than $1,000 in 2023, when student loan cancellations started climbing and some borrowers decided to repay their student loan balances prior to interest accruing once again in September 2023. And now that student loan payments—and interest—have resumed, student loan balances are rising again for those still with student loan debt.

But even with student loan repayment resumed, forgiveness sums are massive, and they’ve reached nearly 5 million student loan borrowers so far, roughly 10% of all student loan borrowers in the U.S., according to the Department of Education. In effect, that means that while student loan averages remain statistically elevated versus 2023, so many borrowers being removed from the pool of student loan borrowers entirely has contributed to a dip in overall non-mortgage balances.

There are also signs of other types of consumer debt, like personal loan balances, plateauing in 2024. So although auto and credit card debts get an outsized amount of coverage in the financial media, not all types of debt have increased so sharply, if at all.

The Bottom Line

Non-mortgage debts have declined in 2024, largely due to the cancellation of around $175 billion of student loan debt since 2021. Although those cancellations were focused on a particular set of consumers, the size of the cancellations was large enough to lower overall non-mortgage debts for the first time in at least 15 years, according to Experian data.

This story was produced by Experian and reviewed and distributed by Stacker.