Paying $1,000 a month or more for auto loan payments is becoming more common

Canva

Paying $1,000 a month or more for auto loan payments is becoming more common

A conceptual image showing a financial transaction: one hand holding a small model car and another hand holding a stack of $100 dollar bills

With vehicle prices rising rapidly in the past three years, more Americans are digging deeper to pay for their vehicles. And although most consumers who borrow for their car or truck purchases today still have three-digit monthly payments, making payments each month of $1,000 or more is becoming more frequent. Experian dives into the reasons behind this growing trend.

Higher rates, supply shortages play a starring role in increasing car payments

Supply shortages and higher interest rates impact all aspects of the economy, as omelet aficionados were reminded when egg costs doubled earlier this year. But the way we finance our daily driver is a bit different than the way we buy a dozen eggs. Car payments comprise 7% of a typical consumer’s total spending basket, around $4,800 annually, according to data from the Bureau of Labor Statistics. While some consumers might reluctantly switch from eggs to cereal for a few months to save on groceries, finding similar savings for a car purchase isn’t as simple.

![]()

Experian

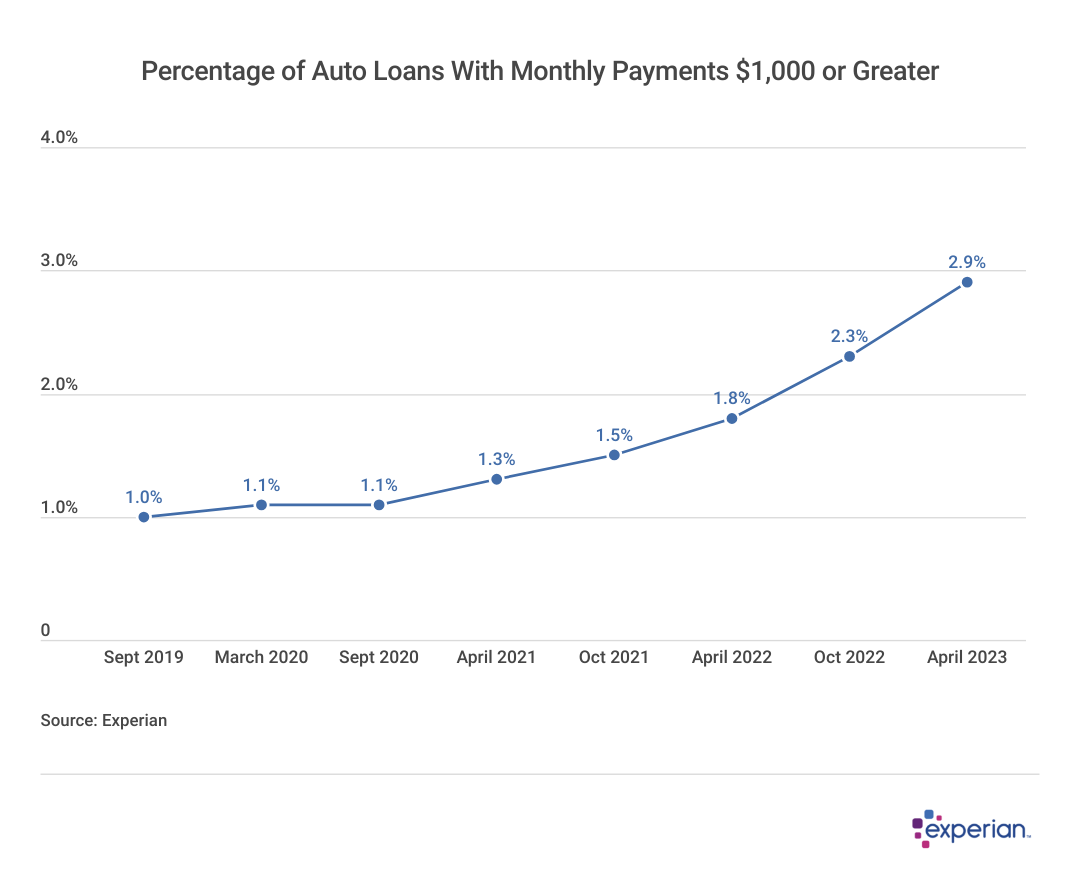

$1,000 or larger monthly payments have nearly tripled since September 2019

A line graph showing the percentage of auto loans with payment over $1000 per month

As of April 2023, there are nearly three times as many consumers willing to pay $1,000 or more for their car or truck than there were in 2019. That’s more than double the average monthly payment of $416, among consumers with a single monthly auto payment, according to Experian data.

What are some of the changes pushing nearly 3% of drivers to pay $1,000 or more now?

Fewer cars, and especially fewer lower-priced cars

Pandemic-induced scarcity is one of the reasons auto financing is much more expensive today. The pandemic interrupted global supply chains, resulting in a constrained selection on dealership lots. Dealers could ask for full sticker price (and sometimes more) for the vehicles they were selling, and many buyers had no choice but to accept. Average new car financing has increased from less than $35,000 prior to the pandemic to over $41,000 today, according to the Experian State of the Automotive Finance Market report from the second quarter of 2023. Furthermore, lower-priced cars—those under $30,000—are becoming less common, as manufacturers focus on higher-cost vehicles, including crossovers, SUVs, and electric vehicles.

Higher APRs for loans

The shortage of automobiles since 2020 may have contributed to higher borrowing rates as well, on top of broader rate hikes from the Federal Reserve. The average APR for a 60-month new auto loan has increased from 4.52% in 2022 to 7.48% as of early 2023, according to Fed data. To finance a new vehicle for $50,000 at those rates, the monthly payment would increase from $932 to $1,001. For those with less-than-good credit scores, where typical APRs are now above 10%, financing even a lower-priced vehicle for five years could result in $1,000 a month car payments.

Experian

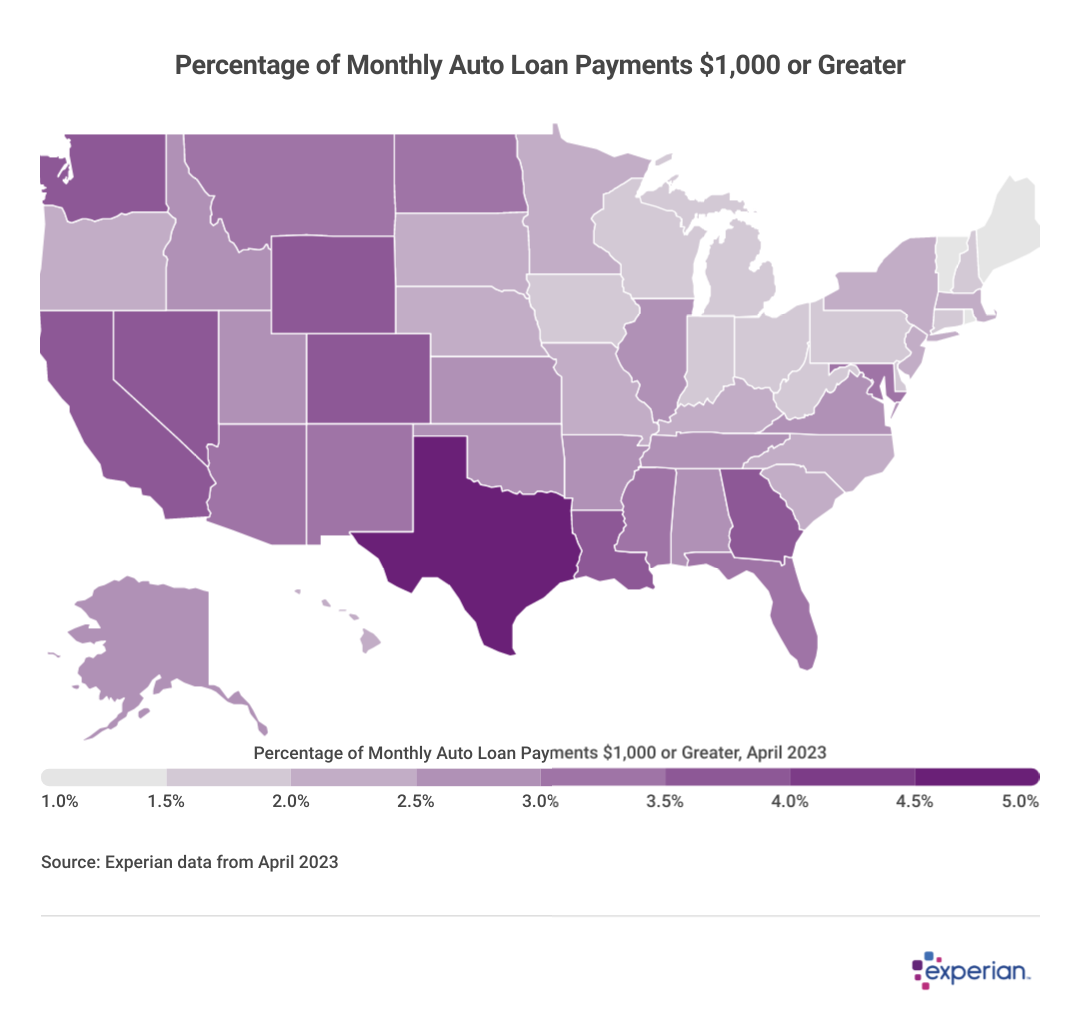

Where drivers are paying $1,000 or more each month

A color coded map of the U.S. showing the percentage of auto loans in each state with payments over $1000 per month

In this analysis, we only looked at consumers with only one auto payment—roughly half of all car loans in 2023—to estimate the percentage of borrowers paying $1,000 or more on a single vehicle in April 2023. (By way of comparison, the average monthly payment for consumers with one car payment is currently $492, somewhat lower than the overall average monthly payment of $612 for borrowers with payments on one or more vehicles.)

Generally, Experian data shows that states with higher average auto loan balances also have high percentages of consumers paying above $1,000 each month for their vehicles. As seen in the map above, rural states like Texas and Wyoming top the list of $1,000-plus monthly payments.

How consumers are compensating

Many more drivers may have been paying more than $1,000 a month as well. However, there’s evidence of increased pushback on higher monthly payments, some of which have their own disadvantages.

- Longer payment terms: Consumers are already averaging close to six years’ worth of payments for either new or used car financing in 2023, and 84- and 96-month financing terms are no longer unheard of. While a longer loan term typically means a lower monthly payment, extending your payments over a longer period means that you’ll have negative equity (in other words, be upside down on your loan) for longer, and will pay more in interest over the life of the loan.

- Deferring new purchases: Federal Highway Administration data shows that America’s fleet of vehicles on the road is aging, suggesting that consumers are squeezing the most out of their existing rides before considering a replacement.

- Refinancing: Consumers who may have initially financed a vehicle purchase with unfavorable rates and later improved their credit may be able to refinance the remaining balance with a local lender and receive improved financing terms.

- Not owning/driving: While it’s still too soon to tell for certain if the trend will persist, it appears that fewer members of Generation Z are driving compared with older generations. The pandemic may have delayed the start of driving for 18- to 26-year-olds, and current data shows that a lower percentage are receiving driver’s licenses or registering vehicles than prior generations.

As though more expensive cars and car payments weren’t bad enough, the cost of insuring vehicles is also going up even more than car and truck prices themselves, according to some measures of insurance premium costs. Americans are on the road, but at a higher cost than ever.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.