Does back-to-school spending increase credit card balances?

Canva

Does back-to-school spending increase credit card balances?

An assortment of school supplies on a green background

September, or August in some parts of the country, is often considered one of the busiest spending months of the year. According to the National Retail Federation (NRF), a trade organization that predicts spending at department stores and other retail outlets, back-to-school spending will produce an additional $130 billion in sales in 2023, a new record for back-to-school season. Many states, for their part, offer sales tax holidays during that time of year to encourage additional local spending.

While it’s easy to see every part of the calendar year as an opportunity to spend, back-to-school spending is often considered second only to end-of-year holiday spending in providing retailers with a sales tailwind. To see if this assumption holds up, Experian reviewed national sales data to see if, in fact, there’s a noticeable impact on consumer spending as summer turns to autumn.

![]()

Experian

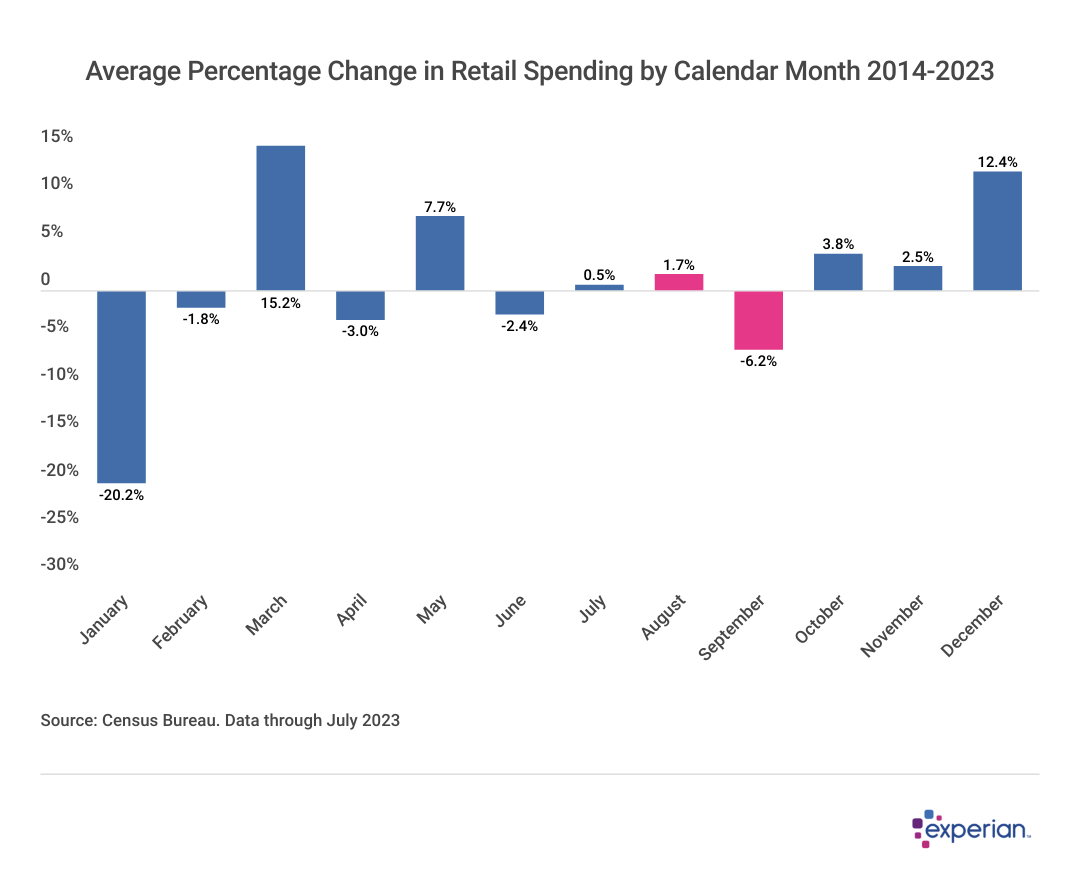

August and September: Busy bees or dog days?

A bar chart showing Average Percentage Change in Retail Spending by Calendar Month 2014-2023

When looking at the past 10 years of retail sales data from the U.S. Census Bureau, August and September don’t seem to be especially huge for retailers. The average change from July to August since 2014 has been a tepid 1.7% increase, which is lower than the last three months of the year. And September shows an obvious decline, where spending is 6.2% lower than it is in August.

There’s at least one obvious reason September retail sales show a persistent decline; it has one fewer day than August, which reduces the opportunity to shop. In addition, September includes the Labor Day holiday, which, despite being as much of an excuse for a sale as most other holidays, isn’t usually considered one of the busiest shopping days of the year.

Experian

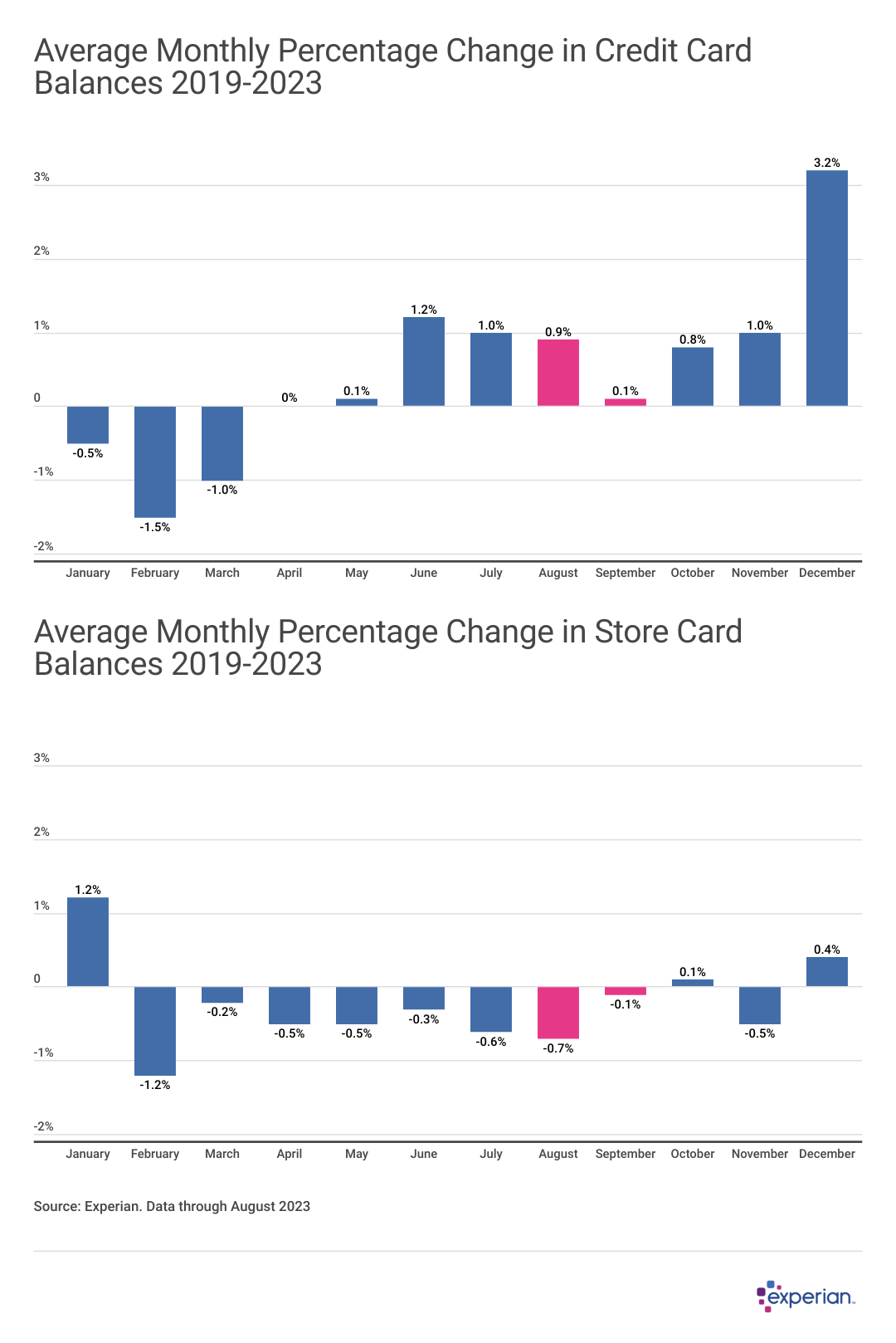

Store card, credit card balances don’t show back-to-school spending upticks

A pair of bar charts showing Average Monthly Percentage Change in Credit Card and Store Card Balances 2019-2023

Looking at recent credit card balance data from Experian, which shows how much card balances shift from month to month, August and September don’t appear to be months where balances substantially increase.

Credit card balances increased an average of 0.9% during August, which is in the middle of the pack as monthly increases are concerned. And since 2019, September balances increased by an average of only 0.1% from the prior August. The usual pattern, as this data confirms, is that consumers spend January, February, and March paying down large balance increases that occur in December, with spending rising or falling modestly for the remaining eight months of the year, including back-to-school season.

Admittedly, this five-year window is a bit limited, as the pandemic resulted in temporary but drastic short-term changes in consumer behavior.

Experian

Federal Reserve data going back 15 years on revolving credit reinforces more recent findings

A bar chart showing Average Monthly Percentage Change in Revolving Credit Balances 2008-2023

Going further back, using data on revolving credit tracked by the Federal Reserve, doesn’t show much difference from the Experian data. August spending increases by 0.7%, on average, while September spending shows a modest decline of 0.2% in revolving credit balances since 2008.

Average credit card balances in September 2023 and beyond

This year, as the business media has repeatedly reminded their audiences, will be different. This is likely to be the case not only for the month of September, but also for the upcoming holiday season, when credit card spending really begins to pick up. The end of 2023 will prove to be challenging for both consumers and retailers for the following reasons:

- Tightened credit: Lenders are becoming choosier about how much credit they extend and to whom, implying that consumers will spend less than in previous years.

- Higher interest rates and APRs: Higher annual percentage rates (APRs) have already increased credit card balances more than they did a year ago. But going forward, higher credit card APRs, currently averaging more than 22%, may result in consumers curbing their spending. Or at least it may shift some of that spending away from interest-accruing card balances to alternative payment plans, like buy now, pay later.

- Student loan payments: They’ll resume in October and may take a significant bite out of the discretionary income student loan borrowers might otherwise use for back-to-school, holiday, and other spending.

So if credit card balances are shown to have increased in September 2023, it will likely be due to accrued interest more than increased spending.

All in all, back-to-school spending, such as it is, may be a bit overhyped, pumpkin spice lattes notwithstanding. But in the coming months, seasonality will likely play a secondary role to larger economic forces.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.